The distributed growth model . A keynote delivered on the invite of the World Bank in Algeria in June 2018

The distributed growth model . A keynote delivered on the invite of the World Bank in Algeria in June 2018

Decade under the UPA I & II can rightly be summed in one line, the ‘Decade of Decay’, in which India had a free fall on all fronts – be it economic failure, diplomatic humiliation, failure of foreign policy, intrusions across borders, corruption & scams or crimes against women. There has been gross misuse & total denigration of government & constitutional institutions and this has eroded the office of the Prime Minister. The Government dithered by each passing day, casting gloom and doom on the country that was once under the NDA regime called the ‘Emerging Super Power’. In 2004, NDA left the Government with 8.1 % growth. The UPA could not even maintain that growth and mismanaged the country so badly, that the growth rate declined to 4.8 %, with the nation in a deep mess. We have lost a wonderful opportunity and have pushed the nation 20 years behind and rendered millions jobless and hopeless.

CAD now exceeds even 1990-91 Level – India is revisiting the crisis of 1991.

Between 2001-02 and 2003-04, the nation had a pleasant experience on balance of payments, turning surplus for continuously three years, which was unprecedented after the post-independence period. All the gains of the NDA period have been frittered away in saving the dynasty rule through various election-financing schemes

Total public debt on India is Rs 4,606,350 crore, and the debt per capita stands at about Rs 38,000

Economy is slowing down and the banks are under strain. Defaults have led to NPAs almost doubling from the 2009 levels. Rs. 2.43 lac Crore of estimated NPAs are in 40 listed banks as on December 2013. Rs.4.0 Lac crore is the amount of restructured loan under the CDR scheme.

The Indian rupee, which was at par with the American currency at the time of Independence in 1947, has touched its historic record low of below 68.80 against the dollar under the UPA

The employment generation actually decreased sharply between 2004-05 and 2009-10, especially when compared to the earlier five-year period.

In the five years from 1999-2000 – 2004-05, NDA created 60.7 million new jobs against the 2.76 million new jobs between the years 2004-05 to 2009-10 under the UPA. Now, India is going to lose more jobs in the coming years due to the wrong policies of the UPA

416 million poor, 316 million illiterate & more than 600 million population without toilets sums up the outcome of the economic policies followed by Congress

India continues to be one of the hungriest nations in the world & accounts for 42 per cent of the world’s underweight children.

India’s Human Development Index rank has a negative trend for the time period 2007-12, which indicates deterioration in the indicators determining the Human Development Index.

Whenever it came to low rate of growth, UPA justified that it was due to global economic situation, but the same cannot be justified for the increasing food prices in India. In November 2013, the Food Prices Index fell by 4.4 % globally, while in India, the Wholesale Price Index (WPI) was estimated to be close to 20 % in November 2013.

On one side, we have European Union’s inflation rate declining to a four-year low, and on the other side, UPA is groping in the dark for the past decade to find a solution for inflation and deficits. Country’s growth that reached near double-digit due to initiatives of the NDA government has come down to 4.5 %, that too remained because monsoons played a face saver and there was a high growth in agriculture ( 4 %). Year 2013 had an unusually good monsoon favoring a good agricultural yield, but had the monsoons been average, the growth would have been below 3 %. It was the agriculture & not the Government Policies that saved the nation from a collapse!

Health and education are defining sectors for equitable human development and sustainable and inclusive economic growth of India.

Despite levying a tax to fund education and enacting a law to ensure access to education for all children between the ages of 6 and 14, the government hasn’t succeeded in improving the learning outcomes in India’s schools, because the UPA thoroughly bungled the Sarva Shiksha Abhiyaan initiated by the NDA.The quality of learning has either shown no improvement or actually worsened in the nine years of the UPA’s rule

Recognized as a critical element for India’s growth, the UPA government had claimed way back in its first term, that 6% of the GDP would be spent on education, which is a bare minimum for an emerging economy like ours. Nonetheless, the sector still stands at around 4% of the GDP today.

It is unfortunate, but the UPA government and the Ministry of Human Resource Development have surely missed the focus on Education and Employment, and the Research & Development expenditure has stagnated under the UPA.

Healthcare is still inaccessible and unaffordable to the masses. Out of pocket spending is still high at 78 %. Goals set forth under NRHM have not been achieved and the scheme has floundered. UPA has failed to deliver health, or healthcare, despite a huge spending.

Due to lack of investment (both public & private) in agriculture, the share of agriculture in GDP has dropped to less than 15%. UPA has failed to increase investment, productivity & profitability of agriculture, leading to farmer suicides, migration from agriculture and widening the urban-rural divide. The Nation is left at the mercy of rain Gods!

The past decade has witnessed, a directionless Indian Foreign Policy under the UPA I & II; of alienation and antagonism in relations with South Asian neighbours, & of international humiliation. India has been miserably failing in accomplishing its national interest due to poor diplomacy

India has slipped to 60th position in terms of its competitiveness globally. This is India’s lowest ever rank and also 31 place below its peer emerging market -China. With regards to GCI, India is placed at 60th position out of 148 economies

India is ranked 134th position out of 189 countries in terms of ease of doing business

Transparency International’s Corruption Perception Index in 2012 ranked India at 94, out of 176 nations

In the global happiness-ranking list, India stands at rank 111-much after Pakistan (rank: 81) and Bangladesh (108).

International rating agencies have been warning that India’s Baa3 rating is in danger of a downgrade, which has vitiated the investment climate. Any further downgrade would club the economy with junk-grade countries.

The fiscal profligacy of the UPA government has put India into a tight corner when it comes to repayment of borrowings. Government bonds worth Rs 1567 billion (Rs 1,56,700 crore) is coming up for redemption in fiscal year 2014-15 & In the fiscal years 2015-16, 2016-17, 2017-18 and 2018-19, government bonds worth Rs 114600 crore, Rs 231200 crore, Rs 256700 crore and Rs 242400 crore are coming up for redemption, respectively.

Erosion of moral and societal values and governance

Crimes & corruption are on the rise across the nation and scams have impacted all the sectors like Panchayat, Housing, Education, Health, Agriculture, Mining, telecom etc. No one is untouched from corruption in the UPA regime

Corruption has become a part of the daily life. There is hardly any day when we do not come across the cases of flourishing corrupt practices getting exposed in one form or another. The policies of UPA have resulted in fast degradation of moral, societal,and cultural values

Use your right to vote to seek a change for a better India

Rajendra Pratap Gupta

On 4th June , 2013 , I analysed the data and concluded that the Indian economy would grow below 4 % when most of our economists were speaking of returning to 6-7 % growth in the second half 2013 . https://commonmansblog.com/2013/06/04/the-titanic-is-sinking-can-we-do-something/

Leading global organizations like IMF / OECD have given similar predictions about Indian economy after 4-5 months of my analysis about the Indian economy

The recent reports of IMF on October 9, 2013 cut the India’s growth to 3.8 % in 2013 http://articles.economictimes.indiatimes.com/2013-10-09/news/42864491_1_world-economic-outlook-growth-forecast-global-growth

Also , OECD stated on 19th November, 2013 that India would grow at 3.4 % http://www.bloomberg.com/news/2013-11-19/oecd-cuts-global-growth-forecasts-on-emerging-market-slowdown.html

On one side , we have European Union’s inflation rate declining to a four-year low ( Mint , 16th November, 2013) and UPA is still groping in the dark to figure out how to handle inflation , deficits and govern this nation

To me , the fate of truck operators & tractors companies and not the sensex, is directly related to the fate of the common man & is the right indicator of the nation’s economic health. Trucks are the means for transporting goods and thereby, the correct parameter to judge the movement of economy. Truck operators are exiting truck business ( Mint, 26th November, 2013)., which is an indicator of the negative economic indicators

Sales of trucks dropped 29% in the first seven months of 2013, and truck sales have been declining for 20 months in a row according to SIAM and the existing truck operators are operating at 40 % of their capacity. Mint dated 26th Nov.

In my view, this mirrors with the growth slowdown of the economy that was once growing more than 8 % and is now growing around 4.5 % ….. High octane speeches of returning to double-digit growth are fine , but when our markets and rupee move with the news of US quantitative easing , it is good enough of the proof, that the intrinsic strength of this country’s economy is weak and of a lesser weightage than just the good news of foreign markets ( tens of thousands miles away ) or the US quantitative easing !

Small truck operators which constitute 75 % of the market are worst hit ( Mint , 26th Nov), and this must be good enough to sum up where have these Oxford, World Bank, IMF famed economists taken this country to ? May be, good rains can shower some temporary good news , but in the short-term and middle term , India has more tears to worry for than merry for this years good rains

No wonder, S&P downgraded IDBI bank debt to junk status . (Nov 26, 2013). More banks are under strain, but I believe that they would not declare NPAs before the next financial year to avoid disclosures that could add to their and the country’s woes !

Please ask the Hon’ble PM to give a statement on a scheme similar to the Food security bill launched with much fanfare in 1975 to reduce malnutrition . This scheme was called the Integrated Child Development Scheme (ICDS) . It has been around for the past 38 years and now again another bill to remove malnutrition ? Despite this scheme being around for about four decades, the scenario is as mentioned below ;

It is a matter of serious concern that the mean per capita consumption of calories has never crossed the minimum threshold for intake ( 2400 Kcal in rural and 2100 Kcal in urban areas), and still about 3/4th of the households do not consumer the minimum calorific intake (Dr.D.K.Taneja, 2013, p. 21)

Protein Energy Malnutrition (PEM) most commonly prevalent in India . 45.3 percent of children under 3 years are under weight as per NFHS -3. Also, as per NFHS-3 , 33 percent of adult women and 28.1 percent of adult men have below normal BMI (Dr.D.K.Taneja, 2013, p. 301)

According to the information procured from the Ministry of Women and Child development via RTI through their letter dated 25 July 2013 ( F. No. 10-1/2011-CD.II(Pt.II)

Total money spend in 11th plan on ICDS was Rs.43829.53 Crore

Total money spent in 2012-13 is 15701.50 crore

During the 12th Five Year Plan, a total approved allocation of Rs. 1,23,580 crore has been made for the scheme. Any additional requirement of funds under ICDS Scheme can be met through Supplementary Demands for Grants and savings. ( Source http://pib.nic.in/newsite/erelease.aspx?relid=93731 )

I think food security bill means ‘another bill for the poor and dollars for the congress’ .

This bill might be another money-making scheme in the name of aam aadmi .. Already, all the FM channels have been bombarded with advertisements for the Food security bill making the intentions of congress very clear that this is a poll gimmick

Rajendra Pratap Gupta

Recently , very few people noticed a four line news that , Moody’s Investor Service downgraded the so-called financial strengths ratings and the baseline credit assessments of;

1. Bank of Baroda

2. Canara Bank

3. Punjab National Bank

The outlook on Union Bank of India has also been changed to negative .

This is the first indicator of ‘Gloom & Doom’ that is set to hit the economy soon. Somehow , India has missed the recession in 2008 , but India will now enter into recessionary phase that is likely to last between 3 -6 years .

Somehow , the investments that came due to ‘overselling’ the India story like the SEZs, power plants , airports are fading off and most of the infrastructure companies are under a huge pile of debt. More NPAs and job losses will follow .

I see that not a single politician or an economist can put his head out and speak the truth that India is hitting a phase of recession ( probably , they do not know it , like the American crisis ). From a high of 9 per cent growth , we are already down by 45 % in our GDP growth . How else do we define recession ? Are we already not into a recession with companies laying off people every month and our growth slowing down by 45 % ?

Let us accept the situation and plan now. Else , India will be headed for an unprecedented crisis. I am not more worried with 2014 election as much as the rapidly falling economy . On many occasions ,i have pointed my friends across political parties that they would be better off losing 2014 elections than winning them , as there is enormous crisis to be faced, and a lot of dirty and hard work to be done to reverse the falling fortunes of this country and it is not going to be an easy 2014 for politics and politicians .

Let us consider this situation ;

India needs foreign exchange – USD . This can come due to ;

Now , exports might start shrinking or remain the same , so not much can be done on that front .

FDI comes in India for

1. Either setting up manufacturing

2. Investment in corporates / stock markets

All the money that comes in FDI needs to produce profits due to either exports or domestic consumption . Both are not going to happen the way investors look at ROI or IRR on their investments as the local consumption story is missing . India has already passed off 100s of millions of poor as ‘middle income aspirational class wanting to spend’ , and this was the biggest fraud of Sonia & MMS led congress government and 100s of corporates have lost millions of dollars every month and are now exiting India or slowing down

Only way the foreigners can make money is dabbling billions of USD in stock markets . So, now FDI’s constitute 11.2 % of GDP in India (2011-12) , and FIIs can play a spoil sport for Indian Economy and generate a balance of payment crisis in any trading hour !

Also, how i could i miss writing about another direct cash transfer scheme of Congress ! Party has got a new way to make money ‘ CSR spending’ under the new companies act .Now politicians can ask corporates for CSR spending and bang ! You know why this bill got passed so easily. And if i am a corporate and i wish to get a license or avoid something OR seeking favours like Robber Vadra, i will give money under CSR to a politician’s NGO….. Wow , another MNAREGA, NRHM and a wonderful legal cash transfer scheme , So who says that XYZ paid bribes , now you cannot prove it , it was just a CSR spending . So, corporates , what are you waiting for , come buy your Rajya Sabha seat , it just cost 100 crores in CSR spending ! Come and block your seats now , it is election year , and sweet -legal deals available through all state leaders and through various national schemes , we have legalised bribes and you have an option to chose your preferred medium . Hurry, this is the last congress government. Hurry up, come , before we run out of time as Elections are likely in November

BTW, time for any sensible politician to come out with a job creation and wealth generation model for India before thinking of FDI or going back to 9 per cent growth

Earlier we realise , the better it is . India is into a recession now !

Rajendra Pratap Gupta

Indian Economy – econoquake waiting to happen, with disastrous seismic cracks

It is a known fact that when symptoms become visible for a chronic disease, complications are tough to treat and the disease is in an advanced stage, but if the disease is diagnosed in earlier stages, the diseases are easy to treat and cure. In India, now symptoms like fiscal deficit, current account deficit, increasing NPAs, inflation, unemployment, lack of investment sentiment, withdrawing of investors etc. are symptoms of a economic earth quake (what I call as econoquake), and it is like a disaster in slow motion for India.

The Indian economy has passed through its worst phase after independence since 2004 and the rot continues to grow.

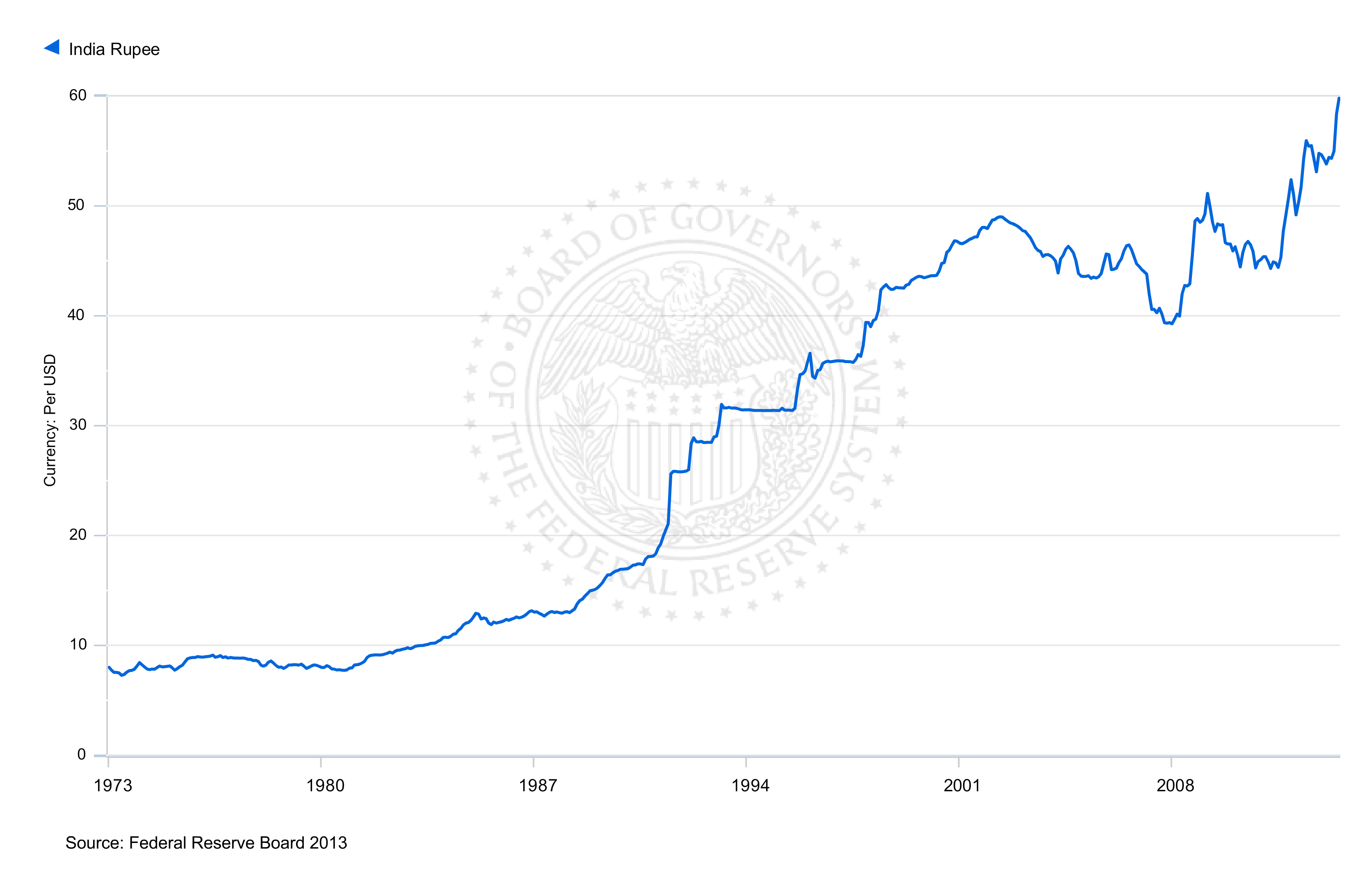

Here are some symptoms that tell how serious is the disease; Indian rupee was trading at 8 Rupee to a dollar in 1973, and has become Rs. 60 to a dollar. Does it not indicate that valuations of this country, and the fact that the economy has weakened by about 750 % in the past 40 years! Ideally, we should have grown and become 1 Rs. to 1 US $, but the poor leadership from these ‘Text Book economists’ (Manmohan Singh, Chidambaram, Montek, Subbarao) have brought down this great nation. Let us analyze a little more in detail

All the data or facts I am quoting are from credible sources and are publicily accessible . (http://blogs.economictimes.indiatimes.com/Whathappensif/entry/rbi-data-shows-how-upa-killed-the-rupee?fb_action_ids=10151534667996725)

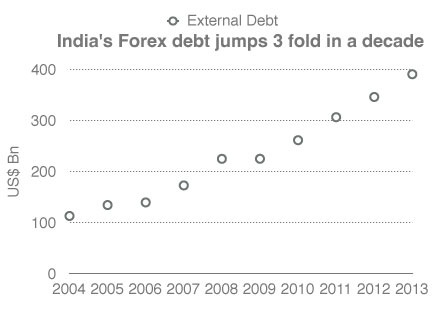

If the 10-year RBI data on short-term foreign debt is analyzed, it is fairly obvious that the UPA destroyed the value of the Rupee. In 2004 when the Vajpayee Government was voted out, the foreign debt at $ 112.4 billion was well covered by the forex reserves. Nine years later it has grown by 350 percent to $ 390 billion and the forex reserves cover falls 25 percent short.

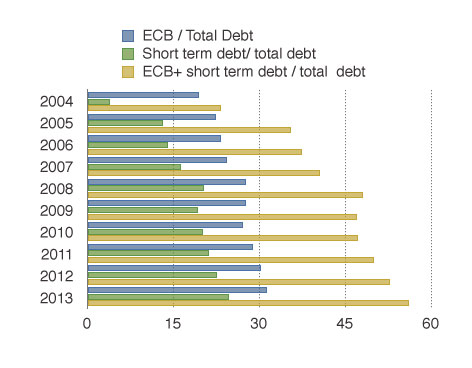

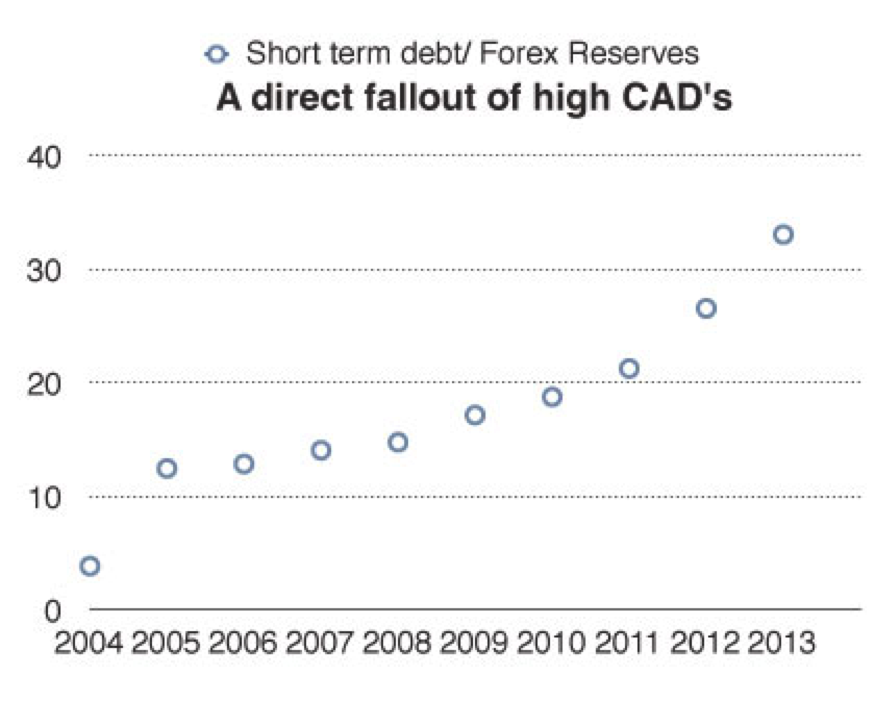

However the rise of foreign debt is not the only reason why the Rupee collapsed from Rs 39 to a dollar to Rs 61 for a dollar during the intervening period. Foreign debt is a necessary evil that is needed by developing countries to push forward their needs to fund foreign capital funded infrastructure. Usually such addition of infrastructure results in long-term asset building that adds to improved productivity of the nation. However in India’s case the rise of external debt has been primarily to fund the current account deficits catering largely to the working capital needs and funded through the short-term loan at higher interest rates. This short-term debt component was very comfortable at just 3.9 percent of the Forex reserves when the NDA was voted out of power nine years ago. By 2009 when the UPA II was re- elected it was around 17.2 percent and by March 2013 the short-term external debt rose to a whopping 33.1 percent of the Forex reserves, which had fallen to $ 292.65 billion. With the reserves further dropping to $ 280.18 billion following RBI’s intervention to stem the Rupee slide in July, the ratio would have worsened.

Short term debts and the External Commercial Borrowings that would need repayment during this FY 2013-14 is high and would cause large outflow of dollars and put pressure on the currency intermittently. For example during May 22 and June 19 there was a net debt outflow of $4.7 billion, one of the prime reasons why Rupee tanked.

These ECB’s and short-term debt have grown to an enormous 56 percent of the total debt by March 2013 almost 2.5 times what they were when the UPA came to power nine years ago. As per RBI data short term debt payable during this Financial year is $ 96.7 billion while ECB’s with 6 month to 1 year maturity that need to be repaid are around $ 21 billion, and NRI deposits maturing during the year are $49 billion. The Rupee is catching a cold because the total foreign debt to be repaid this year works out to a massive $172 billion that is around two-thirds the foreign exchange reserves. Even if interim measures to stop speculation are taking by the RBI it will not address the inherent weakness of the system. Rather it may enhance volatility, as speculative traders if restricted will move offshore to short the Rupee.

Similarly, if we compare our neighbor, China with larger population, Chinese currency has become strong. Though, I must admit, it is not a fair comparison! But the essence is, India is also intervening to control the rupee and Chinese central bank also intervenes, but I guess they have done a better job and the Chinese currency has strengthened compared to US dollar over the past decade and the Indian rupee has not just been weakened, it has been ‘hammered’, and continues to be the worst performing currency in Asia. We can compare Malaysian Ringgit, Singapore dollar or UAE Dirham. All these currencies have strengthened against the Indian rupee

Why rupee will continue to fall?

Domestic markets are failing.

CDR gives an indication that the corporate sector is crashing!

The latest data from the CDR cell suggests that Indian banks added Rs. 15,016 Crore of restructured loans in the March quarter, about Rs. 9,000 Crore less than what they had done in the pre ceding quarter. On a cumulative basis, total restructured loans crossed Rs. 2.27 trillion, or 4.4% of the total loans given by Indian banks.

Gross non-performing assets (NPAs) of 40 listed Indian banks rose to Rs.1.79 trillion in December fromRs.1.25 trillion a year ago, an increase of 43.1%. In the past, the Reserve Bank of India (RBI) had cautioned banks about the need for enhanced risk assessment tools to monitor loan quality.

Defaults in Agricultural credit in another bubble?

A surge in exposure to farm debt through Kisan Credit Cards (KCCs) could emerge as a risk for India’s state-run banks, according to experts.

Subsidized loans are given to farmers through KCCs by state-owned banks. Until March 2012, the outstanding amount on such loans was Rs.1.6 trillion through 20.3 million cards, as per the latest Reserve Bank of India (RBI) data. This may have risen to around Rs.2 trillion, bankers said.

Agriculture is one of the largest sources of bad loans for most banks. It is contributing 9.72% to the gross NPAs of SBI and 7% of Central Bank of India. The nation’s largest lender SBI has the largest gross NPAs —Rs.53, 457.79 Crore, or 5.3% of loans, followed by Punjab National Bank (Rs.13, 997.82 Crore, or 4.61% of loans), Central Bank of India (Rs.8, 938.47 Crore, or 5.64% of loans) and UCO Bank (Rs.6, 711.29 Crore, or 5.53% of loans).

FDI is like mirage for UPA

Government’s efforts to promote India as an investment destination does not seem to be yielding fruits as FDI inflows registered 38 per cent decline to $22.42 billion in 2012-13 compared to the previous year.

It is clear that the UPA government is on the ventilator and no sensible MNC or investor is going to even announce investment for during this government. Knowing well, that the next government will certainly not be either from congress or due to its support. That is one major reason why we have seen in the last week POSCO cancelled its Rs. 30,000 Crore steel plant on July 16th, L.N.Mittal cancelled its Rs. 50,000 Crore steel plant on 17th July 2013. This is a loss of Rs. 80,000 Crore worth of investment committed to India. Normally, when the government is about to be re-elected, we know that practically, all the companies wants to wash its hands in Ganges, and get speedy approvals for obvious reasons. A ‘Needy’ political party in power wants to ‘cash in’ and so does the ‘greedy’ corporates. We have seen how business leaders get national awards like padamshree and padmavibhushan in the election years or the year preceding the election year … but this time, the scene is different. No sensible business house, no matter how ‘greedy’ it is, will commit any investment before the next general elections. So, I see no respite to Indian economy till 2014 end or may be, 2015.

FII’s the real culprits for rupee slide? May be!

FDI Inflows in India and Outflows from India from 2007 to 2012: (amount in US$ billion)

|

|

FDI Inflows to India |

FDI Outflows from India |

||||||||

|

2008-09 |

2009-10 |

2010-11 |

2011-12 |

|

2008-09 |

2009-10 |

2010-11 |

2011-12 |

|

|

|

Total |

43.4 |

35.6 |

27.4 |

36.5 |

|

19.3 |

15.9 |

15.3 |

12.6 |

|

|

As a % of GDP |

3.4% |

2.6% |

1.7% |

2.0% |

|

1.5% |

1.2% |

0.9% |

0.7% |

|

|

FDI Investment Stocks |

125.2 |

171.4 |

204.7 |

203.9 |

|

63.3 |

80.9 |

96.4 |

108.8 |

|

|

FDI Investments Stocks as % of GDP |

9.8% |

12.7% |

12.6% |

11.2% |

|

4.9% |

6.0% |

5.9% |

6.0% |

|

|

Country |

2008-09 |

2009-10 |

2010-11 |

2011-12 |

Total |

2008-09 |

2009-10 |

2010-11 |

2011-12 |

Total |

|

Singapore |

3.42 |

2.38 |

1.70 |

4.31 |

11.81 |

4.06 |

4.20 |

3.99 |

1.86 |

14.11 |

|

Mauritius |

11.04 |

10.34 |

6.98 |

8.92 |

37.28 |

2.08 |

2.15 |

5.08 |

2.27 |

11.57 |

|

Netherlands |

0.85 |

0.90 |

1.21 |

1.16 |

4.12 |

2.79 |

1.53 |

1.52 |

0.70 |

6.54 |

|

USA |

1.80 |

1.94 |

1.17 |

0.91 |

5.82 |

1.02 |

0.87 |

1.21 |

0.87 |

3.97 |

|

UAE |

0.25 |

0.63 |

0.34 |

0.33 |

1.55 |

0.63 |

0.64 |

0.86 |

0.38 |

2.51 |

|

British Virgin Islands |

No data |

No data |

No data |

No data |

No data |

0.00 |

0.75 |

0.28 |

0.52 |

1.55 |

|

UK |

0.83 |

0.66 |

0.76 |

2.75 |

5.00 |

0.35 |

0.34 |

0.40 |

0.44 |

1.53 |

|

Cayman Islands |

No data |

No data |

No data |

No data |

No data |

0.00 |

0.04 |

0.44 |

0.14 |

0.62 |

|

Hong Kong |

No data |

No data |

No data |

No data |

No data |

0.00 |

0.00 |

0.16 |

0.31 |

0.46 |

|

Switzerland |

No data |

No data |

No data |

No data |

No data |

0.00 |

0.00 |

0.25 |

0.16 |

0.41 |

|

Other Countries |

No data |

No data |

No data |

No data |

No data |

7.65 |

3.19 |

2.65 |

1.23 |

14.71 |

|

Japan |

0.41 |

1.18 |

1.56 |

2.75 |

5.90 |

No data |

No data |

No data |

No data |

No data |

|

Cyprus |

1.30 |

1.63 |

0.91 |

1.32 |

5.16 |

No data |

No data |

No data |

No data |

No data |

|

Germany |

0.60 |

0.63 |

0.20 |

1.46 |

2.89 |

No data |

No data |

No data |

No data |

No data |

|

France |

0.46 |

0.30 |

0.73 |

0.47 |

1.96 |

No data |

No data |

No data |

No data |

No data |

References:

(1) OECD data on FDI in Figures as on January 15, 2013.

(2) Zenith International Journal of Business Economics and Management Research, July 2012.

(3) World Investment Report various issues.

(4) If there are any inadvertent errors in the data, it is regretted

Please see how foreigners are investing money in stock markets, and have taken over 100 Billion USD (108.8 Billion dollars, Which is 6 % of India’s GDP) outside India just in one year (2011-12).

How will our Finance Minister address the Balance of payment issue, which needs 75 billion USD?

11 % of GDP is in the hands of FDI / FIIs? Are we safe? Is our growth trickling down or trickling outward? This is in complete deviation of the path of a self-reliant India propounded by our freedom fighters. We are not building a West India company on the lines of the erstwhile East India Company? Time to take a serious look at the data and take concrete actions. It is a wake-up-call for India

Dr.Akash Mehta compiled this data on FII’s on my request. Acknowledged with thanks Dr.Mehta.

Vehicle sales – another symptom of the anemic economy

Car sales in India fell for a record eighth month in row in June with a dip of 9 percent as economic slowdown and low consumer sentiments continue to hit demand, prompting industry body SIAM to seek stimulus package for the automobile sector from the government.

With actual sales in the first quarter of this fiscal turning out to be wide off the mark from what it had forecast in April, Society of Indian Automobile Manufacturers (SIAM) stayed away from revising sales projections it had made in April this year and stated that even those targets were unlikely to be met, except in two-wheeler segment.

According to the latest figures, domestic car sales stood at 1,39,632 units in June as against 1,53,450 units in the same month last year.

We know the problem. So what next?

India has focused too much on FDI / FII’s to bring in dollars, and the capitalists countries are like Shylock (Merchant of Venice). They will extract their pound of flesh. So, India got quick dollars from FII’s, and FII’s made quicker returns and exited the markets and today FIIs have 11 % of the investment in stocks, as I have given the data above. The fact is that, a clutch of foreign investors can destabilize India by withdrawing their investment. FIIs are short-term hedgers and they damage infringe long-term damage to our currency & country. Small retail investors become bankrupt because of FIIs. What came out as a myopic solution to our fiscal deficit and balance of payment crises has today turned into a major national security issue?

Economic Competitiveness: We need to focus on economic competitiveness. We have lost in the last few decades.

Areas to focus, agriculture – we need to amulify agriculture (taking a cue from Amul’s experiment of cooperative movement in milk). We need to support farmers. Make a paradigm shift in modernizing agriculture, training, and equipping farmers to set up SME food processing units. This should make us the top most processed food country in the world in the next decade. The national highways project of Shri. Vajpayee (Golden Quadrilateral Project) was the best step taken since independence for inclusive growth, and this must be pursued aggressively. During NDA regime the road building was 20 KMs a day and under UPA it is down to a KM or two. The Atal Behari Vajpayee government bequeathed a robust economy to the UPA. Remember that the growth rate registered in 2003-04, the last year of the NDA regime, was an impressive 8.5%. Foreign exchange reserves were plentiful. General prices were well under control. Share markets were booming. And there was a general sense of well-being. Work on the Golden Quadrilateral highway linking four corners of India was on in full swing. And various public infrastructure projects under the Public-Private-Partnership model were proceeding without any hitch.

Now, in the last year of the UPA-II, we are back to the Hindu rate of growth. If the economy logs anything above 5% it would be a miracle

(http://www.sunday-guardian.com/analysis/back-to-where-the-economy-was-during-the-early-90s)

My personal prediction is, that we will be below 4 % in growth soon if the regime continues the same way and I have predicted it long back

(https://commonmansblog.com/2013/06/04/the-titanic-is-sinking-can-we-do-something/)

Tourism- spiritual tourism – Tourism is the next best bet after agriculture and we must focus on it by innovating in this sector. I have detailed plan for creating millions of jobs and billions of dollars through employing matriculate youths in this sector.

Intellectual property (IP): India has become a sweatshop and nothing wrong in it, but we need to focus on building IP in science, technology, defense, & agriculture. It is shame that India has not even built a software platform (operating system) and still relies on Microsoft and IOS. Indians in software arena should take a challenge and build the best operating system rather than spending billions of dollars buying MS Office and Apple operating system or Google. We need a search engine developed by Indians. India spends billions of dollars on universities but the IP registered by just one company Texas Instruments (for the sake of giving example I am quoting Texas Instruments) from its Bangalore office might exceed the patents granted to researchers in Indian universities. We need a complete over haul in our education systems that give the world the most valuable IPs, which can be monetized.

Geographical indicators (GI’s): We all are aware that many Geographical Indications like Darjeeling Tea, Mysore Silk, and Champagne across the world have become premium global products. While protection of GIs is very important, it is all the more important to extract economic benefit out of registered GIs. In India we have 184 Indian GIs has been registered till now but hardly a few of them have accessed global market.

On the other hand we are also seeing growing number of GIs from other countries like Peruvian Pisco, Scotch whisky, Cognac, Prosciutto de Parma, Tequila etc. have registered in India.

While it is understood that not every Indian GI has the potential of capturing global market, but many of them have. However we have not seen enough initiative and support system for such promising GIs having healthy export market. There must be a plan to build on the legacy of these GI’s, and targeted GI must be turned into a USD 10 billion global markets for Indians.

Boost manufacturing with a focus on SME’s: Women’s employment has taken an alarming dip in rural areas in the past two years, a government survey has revealed. In jobs that are done for ‘the major part of the year’, rural women lost a staggering 9.1 million jobs. This emerges from comparing employment data of two consecutive surveys conducted by the National Sample Survey Organization (NSSO) in 2009-10 and 2011-12. NDA, during 1999-2004, 60.7 million jobs were created while UPA Government, during 2004-2009, created only 2.7 million jobs. (Data source: National Sample Survey Office).

Organic farming, Herbals & Nutraceuticals: The whole world is moving to traditional and complimentary medicine and India has a scientific traditional medicine dating back to 5000 years. We can create rotation farming for herbals and organic foods and create millions of jobs and billions of dollars worth of exports.

Foreign policy: Neighbors can help. We need not be hooked to G8 / 14/ 20. It is time to have a strategic alliance in Asia, A-2 (India and China) on the lines of G-4, we need to create A-4, the big 4 Asian economies must come together to lead Asia. This is where India must initiate moving from G-20 to A-4.

Lastly, it would not be wrong to say that lakhs of small and medium enterprises , and even 27 big corporate houses have 41 trillion rupee debts (http://www.livemint.com/Companies/7TnLNfHilL2UOkPVNku8UM/Kumar-Mangalam-Birla-is-the-highestpaid-director.html ) . So , this is a steriod induced survival for most of the corporate entitites be it small or big .More pain is expected by this year end. So the government needs to keeps its head low and overheads lower and find solutions to avoid NPA’s . Though, it is an another thing, that UPA has in itself become an NPA.

Rajendra Pratap Gupta

Global Economic Outlook 2013

http://www.conference-board.org/data/globaloutlook.cfm

The global economy has yet to shake off the fallout from the crisis of 2008-2009. Global growth dropped to almost 3 percent in 2012, which indicates that about a half a percentage point has been shaved off the long-term trend since the crisis emerged. This slowing trend will likely continue. Mature economies are still healing the scars of the 2008-2009 crisis. But unlike in 2010 and 2011, emerging markets did not pick up the slack in 2012, and won’t do so in 2013. Uncertainty across the regions – from the post-election ‘fiscal debate’ question in the U.S. to the Chinese leadership transition and reforms in the Euro Area – will continue to have global impacts in sluggish trade and tepid foreign direct investment.

Main results:

Global Outlook for Growth of Gross Domestic Product, 2013-2025 (May 2013)

Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia & Herzegovina, Croatia, Macedonia, Serbia & Montenegro, and Turkey.

Source: The Conference Board Global Economic Outlook 2013, May 2013 update

Global Outlook for Growth of Gross Domestic Product, 1996-2013 (May 2013)

|

1996 – 2005 |

2006 – 2012 |

2012 |

2013 |

||||||

|

Distribution of World Output 2012 |

GDP Growth |

Contribution to World GDP growth**** |

Projected GDP Growth |

Contribution to World GDP growth**** |

Projected GDP Growth |

Contribution to World GDP growth**** |

Projected GDP Growth |

Contribution to World GDP growth**** |

|

| United States |

18.2% |

3.3 |

0.7 |

1.1 |

0.2 |

2.2 |

0.4 |

1.6 |

0.3 |

| Europe* |

20.3% |

2.4 |

0.6 |

0.9 |

0.2 |

-0.2 |

0.0 |

0.3 |

0.1 |

| of which: Euro Area |

13.8% |

2.2 |

– |

0.7 |

– |

-0.5 |

– |

0.1 |

– |

| Japan |

5.6% |

1.0 |

0.1 |

0.2 |

0.0 |

0.6 |

0.0 |

0.8 |

0.0 |

| Other advanced** |

7.2% |

4.0 |

0.3 |

3.0 |

0.2 |

2.2 |

0.2 |

2.8 |

0.2 |

| Advanced Economies |

51.3% |

2.7 |

1.7 |

1.2 |

0.7 |

1.1 |

0.6 |

1.2 |

0.6 |

| China |

16.4% |

8.1 |

0.6 |

10.4 |

1.3 |

7.8 |

1.2 |

7.5 |

1.2 |

| India |

6.3% |

6.5 |

0.3 |

7.8 |

0.4 |

5.5 |

0.3 |

4.7 |

0.3 |

| Other developing Asia |

5.3% |

3.9 |

0.2 |

5.0 |

0.2 |

5.3 |

0.3 |

5.0 |

0.3 |

| Latin America |

7.7% |

2.8 |

0.2 |

3.7 |

0.3 |

3.1 |

0.2 |

3.0 |

0.2 |

| Middle East |

3.7% |

4.6 |

0.1 |

4.3 |

0.2 |

5.5 |

0.2 |

2.2 |

0.1 |

| Africa |

3.3% |

4.6 |

0.1 |

4.7 |

0.1 |

3.7 |

0.1 |

4.2 |

0.1 |

| Russia, Central Asia and Southeast Europe*** |

5.9% |

4.0 |

0.2 |

4.0 |

0.2 |

3.6 |

0.2 |

2.9 |

0.2 |

| Emerging and Developing Economies |

48.7% |

5.0 |

1.8 |

6.5 |

2.8 |

5.5 |

2.6 |

5.0 |

2.4 |

| World Total |

100.0% |

3.6 |

3.5 |

3.2 |

3.0 |

||||

*Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia & Herzegovina, Croatia, Macedonia, and Serbia & Montenegro, and Turkey..

****The percentage contributions to global growth are computed as log differences and therefore do not exactly add up to the percentage growth rate for the world economy.

Source: The Conference Board Global Economic Outlook, May 2013 update.

Comparison of Base Scenario with Optimistic and Pessimistic Scenarios, 2013 – 2025 (May 2013)

|

2013 – 2018 |

2019 – 2025 |

||||||

|

GDP Growth in Optimistic Scenario |

GDP Growth in Base Scenario |

GDP Growth in Pessimistic Scenario |

GDP Growth in Optimistic Scenario |

GDP Growth in Base Scenario |

GDP Growth in Pessimistic Scenario |

Distribution of World Output 2025 |

|

| United States |

2.5 |

2.3 |

2.1 |

2.4 |

2.0 |

1.6 |

18.3% |

| Europe* |

1.5 |

1.2 |

0.8 |

1.6 |

1.3 |

0.9 |

17.4% |

| of which: Euro Area |

1.4 |

1.1 |

0.8 |

1.6 |

1.3 |

1.0 |

12.0% |

| Japan |

1.3 |

0.9 |

0.5 |

1.2 |

0.9 |

0.7 |

4.8% |

| Other advanced** |

3.5 |

2.6 |

1.7 |

2.5 |

1.8 |

1.2 |

7.3% |

| Advanced Economies |

2.1 |

1.8 |

1.4 |

2.0 |

1.6 |

1.2 |

47.8% |

| China |

8.0 |

5.8 |

3.7 |

4.9 |

3.7 |

2.5 |

22.7% |

| India |

5.7 |

4.7 |

3.6 |

4.5 |

3.8 |

3.2 |

8.2% |

| Other developing Asia |

6.4 |

5.0 |

3.6 |

5.5 |

4.4 |

3.2 |

4.9% |

| Latin America |

3.9 |

3.2 |

2.5 |

3.4 |

2.8 |

2.2 |

7.1% |

| Middle East |

2.7 |

2.5 |

2.3 |

2.5 |

2.3 |

2.0 |

2.5% |

| Africa |

5.1 |

4.1 |

3.2 |

5.0 |

4.1 |

3.2 |

2.6% |

| Russia, Central Asia and Southeast Europe*** |

3.1 |

2.1 |

1.2 |

2.1 |

1.5 |

1.0 |

4.1% |

| Emerging and Developing Economies |

5.7 |

4.4 |

3.0 |

4.2 |

3.3 |

2.5 |

52.2% |

| World Total |

4.0 |

3.1 |

2.2 |

3.3 |

2.6 |

1.9 |

100.0% |

*Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia & Herzegovina, Croatia, Macedonia, Serbia & Montenegro, and Turkey.

Source: The Conference Board Global Economic Outlook 2013, May 2013 update

Indian Prime Minister Manmohan Singh said the country’s economic slowdown was cyclical and temporary and that pessimism was unwarranted.

Many economists say hurdles to growth stem from the government’s slow pace of policy reforms as well as the country’s crumbling infrastructure and layers of red-tape.

India’s economic troubles are reflected in its gaping fiscal deficit, persistently high inflation and pessimism among businesses and consumers. This has driven down investments and demand.

Uncertainty in developed markets hasn’t helped. India’s exports, which account for about a fifth of its gross domestic product, have slowed sharply over the past year. Meanwhile, the country’s import bill has swelled, leading to a record-high current account deficit at 6.7% of GDP in the October-December quarter.

Eurozone is a signal that worst is yet to come ?

Unemployment across the 17 European Union countries that use the euro hit another record high in April – and appears to be on course to hit 20 million this year in what would be another gloomy landmark for the currency bloc.

Eurostat, the EU’s statistics office, said on Friday that the unemployment rate rose to 12.2% in April from the previous record of 12.1% the month before. In 2008, before the worst of the financial crisis, it was around 7.5%.

A net 95,000 people joined the ranks of the unemployed, taking the total to 19.38 million. At that pace, unemployment in the currency bloc – which has a population of about 330 million – could breach the 20 million mark by the end of the year.

The unemployment figures mask big disparities among the euro countries. While over one in four people are unemployed in Greece and Spain, Germany’s rate is stable at a low 5.4%.

The differences are particularly stark when looking at the rates of youth unemployment. While Germany’s youth unemployment stands at a relatively benign 7.5%, well over half of people aged 16 to 25 in Greece and Spain are jobless. Italy’s unemployment rate hit its highest level in at least 36 years to over 40%.

“Youth joblessness at these levels risks permanently entrenched unemployment, lowering the rate of sustainable growth in the future,” said Tom Rogers, senior economic adviser at Ernst & Young.

By contrast the US economy has been growing steadily since the end of its recession in June 2009 and the jobs market has started to improve, with the unemployment rate falling to 7.5% in April.

The asset quality is declining in tandem with the economic cycle : http://www.livemint.com/Opinion/JdBQccPTowuvisdqj9guXN/The-deterioration-in-Indian-banks.html

The financial problems of Indian companies are now being reflected in the asset quality of banks that have lent them money.

The disappointing fourth quarter results announced by the State Bank of India in May are perhaps the starkest example of how the financial condition of Indian banks has deteriorated in tandem with the economic cycle. A recent report by India Ratings and Research, an arm of Fitch Ratings, predicts further deterioration—Rs.1.26 trillion of bank loans may potentially be in distress over the next 12 to 24 months, it says.

The Reserve Bank of India (RBI) has done well to begin making it tougher for banks to brush their problems under the carpet. The central bank on Thursday tightened the rules for corporate debt recasts, asking banks to set aside more money for restructured loans as well as making promoters of companies personally liable for loan losses. This follows an earlier decision in November to increase provisioning for restructured assets.

Non-performing loans have been climbing. The problem of restructured assets has also been increasing over recent quarters. The total value of restructured loans in bank books under the corporate debt restructuring facility was an estimated Rs.2.29 trillion in March. There are an additional Rs.1.7 trillion of loans that have been restructured on a bilateral basis between individual banks and their troubled borrowers, according to unofficial estimates.

Such restructured loans as well as the usual bad loans now weigh down bank balance sheets.

The recent moves to raise the cost of loan restructurings—or the withdrawal of regulatory forbearance—is an implicit signal from the central bank that problem loans will not disappear in a jiffy. It usually makes sense to give lenders breathing space to put their loan books in order when companies are hit by a temporary downturn. A few quarters of leniency can help companies get back to their loan repayment schedules quickly. But it is now increasingly clear that the Indian economy is in the midst of a long slowdown, so banks will need to be far tougher with problem loans.

The rise in problem loans should not come as a surprise. It is the inevitable aftermath of a credit boom, as is the case in other economies as well. Loan growth in India was around twice of nominal gross domestic product in the years that immediately preceded the 2008 crisis, a sure sign of effervescent lending. Part of this unusual buoyancy in lending can be explained by the decisions taken within banks but the pressure from New Delhi to step up lending in those exuberant years was also a factor. This is the moment of the inevitable hangover.

What now? A quick improvement seems unlikely. First, it seems that India has still not seen the bottom of the credit cycle. Second, the standard metrics on the ability of companies to service their debt (such as interest cover and free cash flow) are also flashing amber. Third, a sharp reduction in interest rates seems unlikely despite the unexpectedly sharp drop in inflation in recent months. Our assessment is that asset quality in Indian banks will continue to deteriorate for at least a few more quarters (though rising bond prices as a result of a fall in long-term yields could provide some buffer to banks that collectively own more than a quarter of their assets in bonds).

The asset quality of banks is closely related to the state of the underlying economy, which is now in the midst of a structural slowdown. The recent regulatory tightening should be examined against this backdrop, as a recognition of the true state of the Indian economy.

Investors too should welcome the stricter measures, because the regulatory forbearance we saw after 2009 was an attempt to postpone the day of reckoning, when a bank has to take a hit from its problem loans.

FDI inflows declining and rupee depreciating

http://www.thehindu.com/business/Economy/fdi-dips-by-38-to-224-bn-in-201213/article4775276.ece

Government’s efforts to promote India as an investment destination does not seem to be yielding fruits as FDI inflows registered 38 per cent decline to $22.42 billion in 2012-13 compared to the previous year.

FDI inflows were worth $35.12 billion in 2011-12.

The government had taken several policy decisions in the past few months to attract foreign investments. Important among these include allowing FDI in multi-brand retail and civil aviation sectors and seeking legislative approval for increasing FDI cap in insurance and pension sectors.

In March this year, the country had attracted $1.52 billion FDI, taking the total to $22.42 billion in the entire financial year, an official in the Department of Industrial Policy and Promotion (DIPP) told PTI.

Sectors which received large FDI inflows during 2012—13 include services ($4.83 billion), hotel and tourism ($3.25 billion), metallurgical ($1.46 billion), construction ($1.33 billion), automobiles ($1.53 billion) and Pharmaceuticals ($1.12 billion), the official added.

India received maximum FDI from Mauritius ($9.49 billion), followed by UK ($7.87 billion), Singapore ($5.25 billion), Japan ($2.97 billion) and United States ($1.11 billion).

According to industry experts, there is a need to improve business environment in the country.

In November 2012, India attracted FDI worth $1.05 billion, which was two—year low.

India would require around $1 trillion in the next five years to overhaul its infrastructure sector such as ports, airports and highways to boost growth.

Decline in foreign investments could put pressure on the country’s balance of payments and may also impact the value of the rupee.

Rupee declined by 12 paise to end at 11—month low of 56.50 against the US dollar on Friday amid worries over current account deficit and GDP growth.

With FII outflows of $90 million in stocks, RBI’s poor inflation outlook and GDP growth rate falling to decade’s low of 5 per cent pushed the rupee downwards to 56.76 — its lowest since June 28, 2012.

Economic growth rate slipped to a decade low of 5 per cent in 2012—13 due to poor performance of farm, manufacturing and mining sectors.

GDP growth in Jan- March is a mere statistical growth due to base affect ?

Has the economy turned the corner? That’s the big question the gross domestic product (GDP) numbers were supposed to answer. Has it indeed bounced off a bottom? At first glance, the answer to that question seems to entirely depend on your measuring rod. For instance, if we take the quarterly estimates of GDP at 2004-05 market prices from the expenditure side, we find real GDP growth was 3.4% in the June quarter, 2.5% in the September quarter, 4.1% in the December quarter, and 3% in the March quarter. By that yardstick, the economy hit a bottom in the September quarter of 2012-13, bounced back in the next, and then fell back again in the March quarter. The rather dubious consolation is that this yardstick is well known to be dodgy and the credibility of the expenditure-side GDP figures is rather low.

Going back to the more credible GDP data at factor cost, we find growth was 4.8% in the March quarter, a mite higher than the nadir of 4.7% reached in the preceding quarter. That would indicate that the economy has indeed bounced off a bottom, a very weak bounce, more of a twitch really.

The problem, as usual, lies in the base effect. It’s true that real GDP growth at factor cost was 4.7% in the third quarter and 4.8% in the fourth quarter compared with a year ago. That 4.7% growth was on top of 6% growth in the third quarter of 2011-12, while the 4.8% growth was on top of a much-lower 5.1% growth in the fourth quarter of 2011-12. Even the feeble bounce was entirely statistical.

The same holds true for several of the sectors. Growth in manufacturing, for example, has moved up slowly and steadily from minus 1% in the first quarter of 2012-13 to 2.6% in the fourth quarter. That looks like a decent recovery. The problem is that in the first quarter of 2011-12, manufacturing growth was 7.4% and it was a mere 0.1% in the fourth quarter of that year. In short, the entire credit for the growth in manufacturing goes to the base effect.

Apart from agriculture, with its seasonal vagaries, are there any sectors that have bucked the base effect? The financing, insurance, real estate and business services segment seems to have done just that. It grew by 9.1% in Q4, 2012-13, on top of 11.3% growth in the year ago quarter. Compare that to its much-lower 7.8% growth in Q3, 2012-13, on top of 11.4% growth in the year ago quarter.

On the other hand, there are several sectors that have done badly in spite of a favourable base effect. Consider electricity, gas and water supply, whose growth rate has gone down from 4.5% in the third quarter of 2012-13 to 2.8% in the fourth, although growth in this sector in Q4 of the previous year was much lower than in Q3 that year. This clearly shows the impact of supply-side problems in the power sector. Similarly, growth in trade, hotels, transport and communication slackened a bit in the fourth quarter compared with the third, despite a favourable base effect. Community, social and personal services, a proxy for government expenditure, unsurprisingly saw tepid growth as the fiscal deficit came down.

How much did the different sectors of the economy contribute to GDP growth in 2012-13? As much as 35% of the growth was generated by the trade, hotels, transport and communication sector, closely followed by financing, insurance, real estate and business services, which accounted for 31.3%. The community, social and personal services segment contributed 16.8% of the growth. It means these three service sectors contributed a huge 83.1% to growth last fiscal year.

Contrast the miserable performance of manufacturing, which accounted for a mere 3.3% of growth. The construction sector contributed more than double that. As a matter of fact, agriculture, forestry and fishing generated 5.4% of last year’s growth, more than the share of manufacturing. The contribution of the mining sector was negative, because of the court-directed closure of mines. The chart shows the contribution from the different sectors. Clearly, mining is the weakest link, closely followed by manufacturing.

The Central Statistical Organisation also seems to have been bang on target with its estimate of 5% real GDP growth at factor cost for 2012-13. A closer examination shows, however, that it had overestimated growth in manufacturing, mining, electricity, gas and water supply and, to a minor extent, in community, social and personal services, and underestimated growth in trade, hotels, transport and communication. That the overall growth rate came out exactly as it predicted can be attributed to an extraordinary stroke of luck.

India’s growth slows down – India is running out of fuel ?

The Indian economy grew at its slowest pace in a decade in 2012-13, posing another fresh challenge for the UPA coalition to revive growth and boost sentiment ahead of the general elections next year.

Data released by the Central Statistical Organization (CSO) on Friday showed that the economy grew 5% in 2012-13, compared to 6.2% expansion in the previous year. It was in line with the advanced estimates released earlier.

The economy grew 4.8% in the January-March period, the fourth quarter of the 2012-13 fiscal year, marginally above the upwardly revised 4.7% expansion in the previous quarter, providing some hope of a tentative turnaround. But the overall economic scenario still remains challenging and the GDP data should come as a wake-up call for the government.

The CSO numbers are also an embarrassment for the finance ministry which had questioned the statistics office’s methodology and expressed doubts about the advanced estimates.

The finance ministry had slammed the CSO for forecasting 5% growth for 2012-13. Finance minister P Chidambaram had said the estimate of 5% was based on “dated data”. He had said that growth would be closer to 5.5% and had exuded confidence that green shoots of recovery were visible in the economy.

The high current account deficit, which widened to 6.7% in the December quarter, and stubborn inflation has acted as obstacles to easing monetary policy aggressively. While the Reserve Bank of India has cut interest rates it has cautioned about the persisting inflationary pressures and risks still facing the economy.

What has been most disappointing is that industrial output growth in 2012-13 has been a mere 1%, posing a threat to job creation and overall growth.

Friday’s data showed the farm sector rose 1.9% in 2012-13 compared to 3.6% in the year-ago period while the crucial manufacturing sector grew 1% compared with 2.7% expansion in 2011-12.

The services sector, which accounts for nearly 60% of the economy, rose 7.1% in 2012-13 compared to 8.2% growth in the year-ago period.

CDR gives an indication that the corporate sector is crashing !

The latest data from the CDR cell suggests that Indian banks added Rs. 15,016 crore of restructured loans in the March quarter, about Rs. 9,000 crore less than what they had done in the pre ceding quarter. On a cumulative basis, total restructured loans crossed Rs. 2.27 trillion, or 4.4% of the total loans given by Indian banks.

Indian banks have been hit by a surge of bad loans in the face of declining economic growth, estimated at a decade’s low of 5% in the year ended 31 March, project delays and high interest rates that have made it difficult for borrowers to repay debt. Lenders have been easing repayment terms to avoid classifying them as bad assets.

The CDR numbers do not reflect the actual pile-up of restructured loans in the banking system because lenders also recast loans outside the CDR platform, on a bilateral basis.

The aggregate figure for bilateral loan recasts is not available, but bankers said such recasts may nearly equal the CDR figure. That would take the total restructured assets of the Indian banking industry to around Rs.4 trillion.

In the whole of fiscal 2012-13, Indian banks restructured a total of Rs.77,101 crore of loans through the CDR route, nearly double the amount in the previous fiscal (Rs.40,000 crore). Analysts expect about 25-30% of such loans to turn bad.

Iron and steel contributed most to the restructured loan pile—23%—followed by infrastructure (9.65%) and power (8.13%). The textile, telecom and fertilizer sectors, and non-banking finance companies, too, are high on the list.

Despite a decline in the CDR numbers in the March quarter, bankers and financial sector analysts are sceptical about a sustainable revival at Indian companies. The pain associated with mounting bad loans is unlikely to ease at least in the next six months, they said.

Gross non-performing assets (NPAs) of 40 listed Indian banks rose to Rs.1.79 trillion in December fromRs.1.25 trillion a year ago, an increase of 43.1%. In the past, the Reserve Bank of India (RBI) had cautioned banks about the need for enhanced risk assessment tools to monitor loan quality.

Factory output shrinks 1st time in over 4 years .

http://in.reuters.com/article/2013/06/03/india-manufacturing-pmi-idINDEE95203N20130603

The sombre PMI findings came hard on the heels of data released on Friday that confirmed Asia’s third largest economy grew at its slowest pace in a decade in the fiscal year that ended in March.

The overall HSBC Manufacturing Purchasing Managers’ Index (PMI), which gauges business activity in Indian factories but not its utilities, sank to 50.1 in May from 51.0 in April, and was the third straight monthly fall.

Though the May reading was the lowest since March 2009, the overall index has held above the watershed 50 level that divides growth from contraction for over four years.

The reading for the factory production sub-index, however, showed output contracted in May from a month earlier as new orders growth slowed to a trickle. The output sub-index fell to 48.6 in May from 50.2 in April.

“Economic activity in the manufacturing sector slowed further in May as output contracted in response to softer domestic orders,” said Leif Eskesen, an economist with survey sponsor HSBC. Eskesen said power outages added to the drop in production

Defaults in Agricultural credit in another bubble ?

A surge in exposure to farm debt through Kisan Credit Cards (KCCs) could emerge as a risk for India’s state-run banks, according to experts.

Subsidized loans are given to farmers through KCCs by state-owned banks. Until March 2012, the outstanding amount on such loans was Rs.1.6 trillion through 20.3 million cards, as per the latest Reserve Bank of India (RBI) data. This may have risen to around Rs.2 trillion, bankers said.

Bad loans may be piling up at banks, but they don’t reflect on the books as the credit limit on such cards keeps increasing. Even if a borrower fails to pay up and the banks add the unrealized interest to the exposure because of the rising credit limits—typically 10% every year—the so-called capitalization of interest does not affect the status of the loan account.

State Bank of India (SBI) has the largest exposure to KCC loans—about Rs.44,000 crore— and 5% of this has turned bad, the bank said; Central Bank of India’s exposure isRs.8,428.05 crore and that of Bank of Maharashtra is Rs.2,045 crore.

According to RBI data, banks had Rs.33,200 crore overdue in the direct agrifinance portfolio till 2011 June. The latest figures are not available.

The credit culture in rural India deteriorated sharply after the government announced a Rs.70,000 crore debt waiver for farmers in the February 2008 budget.

The farm loan waiver was one of the United Progressive Alliance government’s key programmes in its first tenure and at least partly responsible for its return to power in 2009.

“Outstanding KCC loans have grown at around 33% in past two years while the number of credit cards has grown at around 13%,”

The share of agriculture, which once generated maximum jobs, has been shrinking as a percentage of national income in Asia’s third largest economy—from 35.75% in 1981 to 16.75% in 2012.

Agriculture is one of the largest sources of bad loans for most banks. It is contributing 9.72% to the gross NPAs of SBI and 7% of Central Bank of India. The nation’s largest lender SBI has the largest gross NPAs —Rs.53,457.79 crore, or 5.3% of loans, followed by Punjab National Bank (Rs.13,997.82 crore, or 4.61% of loans), Central Bank of India (Rs.8,938.47 crore, or 5.64% of loans) and UCO Bank (Rs.6,711.29 crore, or 5.53% of loans).

A bad monsoon could mean a dramatic turn for the worse as the June-September rainy season constitutes India’s main source of irrigation.

Brief summary :

And the NPA’s are growing every hour.

10. Gross non-performing assets (NPAs) of 40 listed Indian banks rose to Rs.1.79 trillion in December fromRs.1.25 trillion a year ago, an increase of 43.1%.

11. The total restructured assets of the Indian banking industry could be around Rs.4 trillion.

12. All the emerging or the sunrise industries are not earning enough to pay loans and this clearly shows that India is a oversold story . Iron and steel contributed most to the restructured loan pile—23%—followed by infrastructure (9.65%) and power (8.13%). The textile, telecom and fertilizer sectors, and non-banking finance companies, too, are high on the list.

13. Eurozone is passing through a crises that could worsen, and impact the Indian exporters

14. Rupee is depreciating, and is the worst performing currency in Asia

Overall, I stand by my assessment of the Indian economy in March 2012 (https://commonmansblog.com/2012/03/22/have-we-oversold-the-india-story/ ) and in October 2012 (https://commonmansblog.com/2012/10/11/india-from-emerging-to-a-submerging-economy/ )that India is an oversold story and should prepare for the worst times ahead . Also, I said on my blog in March about India facing a security threat , and we know what China did (https://commonmansblog.com/2013/03/03/economy-downgrade-and-downfall-both-are-a-foregone-conclusion/) .

I see no reason to believe that India will be back to normal before 2015-16, and that too, provided politicians become realistic . In the current environment , none of the political parties or the politicians have a plan to salvage the situation, and my prediction is , that India’s growth rate might fall below 4 % . The Indian Titanic is in mid of a turbulent sea, heading towards a more severe storm . The Titanic is sinking . Can we do something ?

Rajendra Pratap Gupta

On 8th February , 2013, i wrote about the ‘Oxytocin’ injections that the Government is giving to our economy to draw out milk…….here is the proof.

Life Insurance Corporation was the most dependable automated teller machine for the government in the past year, buying record amounts of bonds and stocks of public-sector firms. Which was shown as ‘successful divestment by the Government’.

The state-run insurer’s purchase of government bonds rose 20%, and it bought nearly 40% of the shares sold via offer for sale (OFS) in four out of total seven PSUissues, said people familiar with the investments.

Of the Rs 4.67 lakh crore raised by the government through securities, LIC provided over Rs 1.10 lakh crore, or 21.4% of the total figure.

LIC invested Rs 236 crore in Nalco (35% of the OFS size), Rs 142 crore in RCF (45%), Rs 608 crore in Hindustan CopperBSE 0.87 % (44%), Rs 923 crore in NTPCBSE -0.35 % (5%), Rs 1,069 crore in SAIL (71%) and Rs 282 crore in NMDCBSE 2.50 % (4.7%).

LIC had contributed 81% to the government’s Rs 14,000-crore mop-up from share sales in 2011-12 by investing Rs 11,400 crore in ONGC

LIC invests in government securities with a view to holding them till maturity, and mark-to-market losses in the interim are not good. It would be a good practice to evaluate returns on redemption each time it happens and compare it with benchmark government bond rates. “Any shortfall in the return should be compensated by the government,”

Also, LICs mandate to invest 50 % in Government securities should be re-looked .

So the big question is , was this really divestment or a ‘back door buyout’ & a ‘face saver’ from a state controlled financier with public money, which could have yielded better returns had the LIC invested into blue chip companies . We all know that the state run PSUs will perform poorly when compared to other blue chip firms . Does it not warrant a CAG inquiry into the management ( mismanagement ) of LICs investments under duress ( from Chidambaram ) ?

LIC is failing in its fiduciary responsibilities to its investors ( people of this country who buy insurance policies from LIC ) , who invest Rs. 450 crore a day in LIC . Time to raise this issue and realise , that the actual divestment figure shown by the Government was a back door forced buyback by a family firm ( Government’s family firm- LIC )

Rajendra Pratap Gupta

I am not an economist , so in case, my predictions go wrong ( so far, i have not been wrong on a single occasion ), i do have an option to take refuge in my lack of educational qualifications in the Economic theory unlike the proficient doctors of economics do at PM’s office , Planning Commission & the Finance ministry …..

My belief is that in 2013-14;

1. This Government will struggle to revive growth

2. Inflation ‘might’ ( 50 % chances ) come down a bit , as consumption story of India will go down

3. Manufacturing sector will slow down

4. Fiscal deficit will increase, and might create a balance of payments problem , or the Government will open more avenues for FDI ( or bend to the demands of the industrialists )

5. Tax collections will go down

6. Divestment target will not be met under the current situation unless some more ‘targets’ are divested

7. India might face a ‘security threat’ before the next elections

8. Investor confidence cannot be revived due to ‘Governance deficit’ and ‘Scamful’ Government at the centre .

Also, you can expect this Government to come out with injecting ‘Oxytocin’ in the economy as mentioned in my earlier blog ….. but this will be a short-term story, and will further dent the strength of the economy

Overall, not a good omen for job seekers and this nation . Hopefully, this will be the last budget for Congress

Rajendra Pratap Gupta

India presses the ‘Panic Button’

India needs USD 80 Billion of foreign capital to fund its current account gap. Imagine, finance minister Chidambaram doing a road show in Hong Kong to woo investors! Anand Sharma twisting the rules to get IKEA money & pushing for getting dollar funds via FDI in retail, Pranab shunted to Rashtrapati Bhawan & the Vodafone tax amendment being redone..Do all these not appear as desperate measures? I wrote a few weeks ago, on how the ministries are making plans without money, and this is happening for the first time in history…

If the country has strong fundamentals, why should the finance minster be doing a road show in the first place! The panic does not end here, the budget cuts in important sectors like defense and other social sectors does signal that all is not well within India, and the panic button has already been pressed! We are nearing a ‘Fiscal slide’ & the consequent ‘hard landing’ will be steeper than the ‘fiscal cliff’ of the US. We are back to the 90’s. That time also, on the pressure of IMF, we had to ‘open’ the economy. Now the countries that ‘forced’ India to open the economy are also in the same boat ….So now the veiled threat of down grades.

This Government has not addressed the problems of India, as they have not diagnosed the problem rightly …….Our finance ‘doctors’ are just ‘suppressing the symptoms’ and not trying to ‘address the cause’, & So, the disease will never get cured. More pain in store for the Indian Economy

I hope we do not go the Kingfisher way………….

Rajendra Pratap Gupta