Global Economic Outlook 2013

http://www.conference-board.org/data/globaloutlook.cfm

The global economy has yet to shake off the fallout from the crisis of 2008-2009. Global growth dropped to almost 3 percent in 2012, which indicates that about a half a percentage point has been shaved off the long-term trend since the crisis emerged. This slowing trend will likely continue. Mature economies are still healing the scars of the 2008-2009 crisis. But unlike in 2010 and 2011, emerging markets did not pick up the slack in 2012, and won’t do so in 2013. Uncertainty across the regions – from the post-election ‘fiscal debate’ question in the U.S. to the Chinese leadership transition and reforms in the Euro Area – will continue to have global impacts in sluggish trade and tepid foreign direct investment.

Main results:

- Across the advanced economies, the Outlook predicts 1.2 percent growth in 2013, compared to 1.1 percent in 2012. The slight uptick is largely due to Europe, which is expected to return to very slow growth of 0.3 percent after the -0.2 percent contraction in 2012. U.S. growth is expected to fall from 2.2 percent in 2012 to 1.6 percent in 2013.

- In the medium-term, the outlook expects the U.S. and other advanced economies to go some ways toward closing large output gaps – that is, the difference between current output and the level of output an economy can produce in a noninflationary way, given the size of its labor force and its potential to invest in and create technological progress. The current output gap is a result of weak demand due to the 2008-2009 crisis. This development should allow the U.S. to average 2.3 percent annual growth during 2013-2018 before falling to 2.0 percent in 2019-2025. In the same two periods, Japan is expected to grow at 0.9 percent per annum.

- A more significant slowdown is expected for less mature economies over the next year – and beyond. Overall, growth in developing and emerging economies is projected to drop from 5.5 percent in 2012 to 5.0 percent in 2013, with growth falling in China from 7.8 to 7.5 percent and in India from 5.5 to 4.7 percent. From 2019-2025 emerging and developing countries are projected to grow at 3.3 percent.

- The long-term global slowdown we project to 2025 will be driven largely by structural transformations in the emerging economies. As China, India, Brazil, and others mature from rapid, investment-intensive ‘catch-up’ growth to a more balanced model, the structural ‘speed limits’ of their economies are likely to decline, bringing down global growth despite the recovery we expect in advanced economies after 2013.

StraightTalk®

Global Outlook for Growth of Gross Domestic Product, 2013-2025 (May 2013)

Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia & Herzegovina, Croatia, Macedonia, Serbia & Montenegro, and Turkey.

Source: The Conference Board Global Economic Outlook 2013, May 2013 update

Global Outlook for Growth of Gross Domestic Product, 1996-2013 (May 2013)

|

|

1996 – 2005

|

2006 – 2012

|

2012

|

2013

|

|

Distribution of World Output 2012

|

GDP Growth

|

Contribution to World GDP growth****

|

Projected GDP Growth

|

Contribution to World GDP growth****

|

Projected GDP Growth

|

Contribution to World GDP growth****

|

Projected GDP Growth

|

Contribution to World GDP growth****

|

| United States |

18.2%

|

3.3

|

0.7

|

1.1

|

0.2

|

2.2

|

0.4

|

1.6

|

0.3

|

| Europe* |

20.3%

|

2.4

|

0.6

|

0.9

|

0.2

|

-0.2

|

0.0

|

0.3

|

0.1

|

of which:

Euro Area |

13.8%

|

2.2

|

–

|

0.7

|

–

|

-0.5

|

–

|

0.1

|

–

|

| Japan |

5.6%

|

1.0

|

0.1

|

0.2

|

0.0

|

0.6

|

0.0

|

0.8

|

0.0

|

| Other advanced** |

7.2%

|

4.0

|

0.3

|

3.0

|

0.2

|

2.2

|

0.2

|

2.8

|

0.2

|

| Advanced Economies |

51.3%

|

2.7

|

1.7

|

1.2

|

0.7

|

1.1

|

0.6

|

1.2

|

0.6

|

|

|

|

|

|

|

|

|

|

|

| China |

16.4%

|

8.1

|

0.6

|

10.4

|

1.3

|

7.8

|

1.2

|

7.5

|

1.2

|

| India |

6.3%

|

6.5

|

0.3

|

7.8

|

0.4

|

5.5

|

0.3

|

4.7

|

0.3

|

| Other developing Asia |

5.3%

|

3.9

|

0.2

|

5.0

|

0.2

|

5.3

|

0.3

|

5.0

|

0.3

|

| Latin America |

7.7%

|

2.8

|

0.2

|

3.7

|

0.3

|

3.1

|

0.2

|

3.0

|

0.2

|

| Middle East |

3.7%

|

4.6

|

0.1

|

4.3

|

0.2

|

5.5

|

0.2

|

2.2

|

0.1

|

| Africa |

3.3%

|

4.6

|

0.1

|

4.7

|

0.1

|

3.7

|

0.1

|

4.2

|

0.1

|

| Russia, Central Asia and Southeast Europe*** |

5.9%

|

4.0

|

0.2

|

4.0

|

0.2

|

3.6

|

0.2

|

2.9

|

0.2

|

| Emerging and Developing Economies |

48.7%

|

5.0

|

1.8

|

6.5

|

2.8

|

5.5

|

2.6

|

5.0

|

2.4

|

|

|

|

|

|

|

|

|

|

|

| World Total |

100.0%

|

3.6

|

|

3.5

|

|

3.2

|

|

3.0

|

|

*Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia & Herzegovina, Croatia, Macedonia, and Serbia & Montenegro, and Turkey..

****The percentage contributions to global growth are computed as log differences and therefore do not exactly add up to the percentage growth rate for the world economy.

Source: The Conference Board Global Economic Outlook, May 2013 update.

Comparison of Base Scenario with Optimistic and Pessimistic Scenarios, 2013 – 2025 (May 2013)

|

2013 – 2018

|

2019 – 2025

|

|

|

GDP Growth in Optimistic Scenario

|

GDP Growth in Base Scenario

|

GDP Growth in Pessimistic Scenario

|

GDP Growth in Optimistic Scenario

|

GDP Growth in Base Scenario

|

GDP Growth in Pessimistic Scenario

|

Distribution of World Output 2025

|

| United States |

2.5

|

2.3

|

2.1

|

2.4

|

2.0

|

1.6

|

18.3%

|

| Europe* |

1.5

|

1.2

|

0.8

|

1.6

|

1.3

|

0.9

|

17.4%

|

of which:

Euro Area |

1.4

|

1.1

|

0.8

|

1.6

|

1.3

|

1.0

|

12.0%

|

| Japan |

1.3

|

0.9

|

0.5

|

1.2

|

0.9

|

0.7

|

4.8%

|

| Other advanced** |

3.5

|

2.6

|

1.7

|

2.5

|

1.8

|

1.2

|

7.3%

|

| Advanced Economies |

2.1

|

1.8

|

1.4

|

2.0

|

1.6

|

1.2

|

47.8%

|

|

|

|

|

|

|

|

|

| China |

8.0

|

5.8

|

3.7

|

4.9

|

3.7

|

2.5

|

22.7%

|

| India |

5.7

|

4.7

|

3.6

|

4.5

|

3.8

|

3.2

|

8.2%

|

| Other developing Asia |

6.4

|

5.0

|

3.6

|

5.5

|

4.4

|

3.2

|

4.9%

|

| Latin America |

3.9

|

3.2

|

2.5

|

3.4

|

2.8

|

2.2

|

7.1%

|

| Middle East |

2.7

|

2.5

|

2.3

|

2.5

|

2.3

|

2.0

|

2.5%

|

| Africa |

5.1

|

4.1

|

3.2

|

5.0

|

4.1

|

3.2

|

2.6%

|

| Russia, Central Asia and Southeast Europe*** |

3.1

|

2.1

|

1.2

|

2.1

|

1.5

|

1.0

|

4.1%

|

| Emerging and Developing Economies |

5.7

|

4.4

|

3.0

|

4.2

|

3.3

|

2.5

|

52.2%

|

|

|

|

|

|

|

|

|

| World Total |

4.0

|

3.1

|

2.2

|

3.3

|

2.6

|

1.9

|

100.0%

|

*Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia & Herzegovina, Croatia, Macedonia, Serbia & Montenegro, and Turkey.

Source: The Conference Board Global Economic Outlook 2013, May 2013 update

Indian Prime Minister Manmohan Singh said the country’s economic slowdown was cyclical and temporary and that pessimism was unwarranted.

Many economists say hurdles to growth stem from the government’s slow pace of policy reforms as well as the country’s crumbling infrastructure and layers of red-tape.

India’s economic troubles are reflected in its gaping fiscal deficit, persistently high inflation and pessimism among businesses and consumers. This has driven down investments and demand.

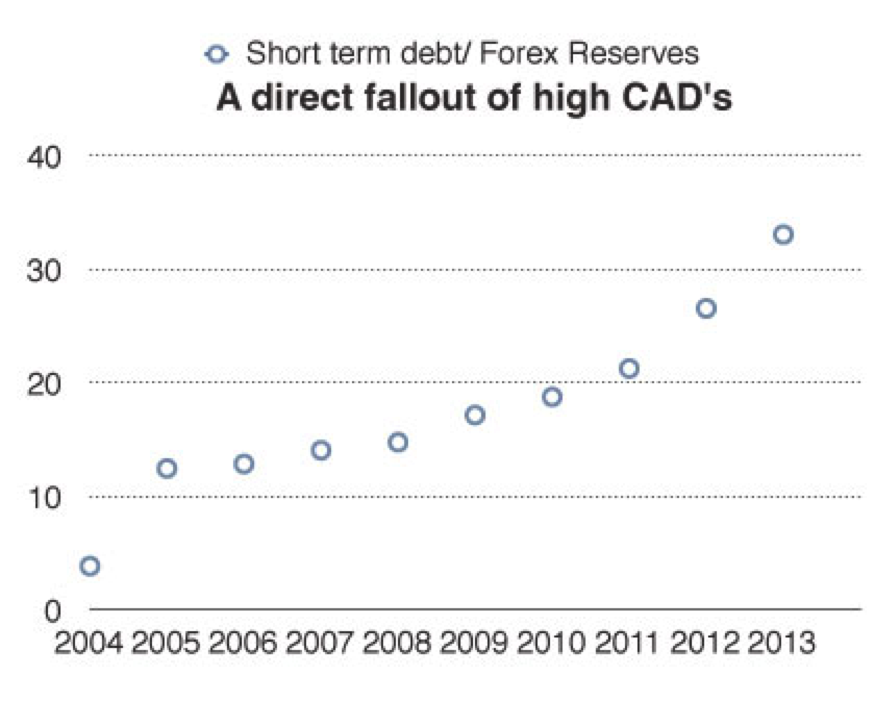

Uncertainty in developed markets hasn’t helped. India’s exports, which account for about a fifth of its gross domestic product, have slowed sharply over the past year. Meanwhile, the country’s import bill has swelled, leading to a record-high current account deficit at 6.7% of GDP in the October-December quarter.

Eurozone is a signal that worst is yet to come ?

http://articles.timesofindia.indiatimes.com/2013-06-01/europe/39673930_1_unemployment-rate-youth-unemployment-unemployment-figures

Unemployment across the 17 European Union countries that use the euro hit another record high in April – and appears to be on course to hit 20 million this year in what would be another gloomy landmark for the currency bloc.

Eurostat, the EU’s statistics office, said on Friday that the unemployment rate rose to 12.2% in April from the previous record of 12.1% the month before. In 2008, before the worst of the financial crisis, it was around 7.5%.

A net 95,000 people joined the ranks of the unemployed, taking the total to 19.38 million. At that pace, unemployment in the currency bloc – which has a population of about 330 million – could breach the 20 million mark by the end of the year.

The unemployment figures mask big disparities among the euro countries. While over one in four people are unemployed in Greece and Spain, Germany’s rate is stable at a low 5.4%.

The differences are particularly stark when looking at the rates of youth unemployment. While Germany’s youth unemployment stands at a relatively benign 7.5%, well over half of people aged 16 to 25 in Greece and Spain are jobless. Italy’s unemployment rate hit its highest level in at least 36 years to over 40%.

“Youth joblessness at these levels risks permanently entrenched unemployment, lowering the rate of sustainable growth in the future,” said Tom Rogers, senior economic adviser at Ernst & Young.

By contrast the US economy has been growing steadily since the end of its recession in June 2009 and the jobs market has started to improve, with the unemployment rate falling to 7.5% in April.

The asset quality is declining in tandem with the economic cycle : http://www.livemint.com/Opinion/JdBQccPTowuvisdqj9guXN/The-deterioration-in-Indian-banks.html

The financial problems of Indian companies are now being reflected in the asset quality of banks that have lent them money.

The disappointing fourth quarter results announced by the State Bank of India in May are perhaps the starkest example of how the financial condition of Indian banks has deteriorated in tandem with the economic cycle. A recent report by India Ratings and Research, an arm of Fitch Ratings, predicts further deterioration—Rs.1.26 trillion of bank loans may potentially be in distress over the next 12 to 24 months, it says.

The Reserve Bank of India (RBI) has done well to begin making it tougher for banks to brush their problems under the carpet. The central bank on Thursday tightened the rules for corporate debt recasts, asking banks to set aside more money for restructured loans as well as making promoters of companies personally liable for loan losses. This follows an earlier decision in November to increase provisioning for restructured assets.

Non-performing loans have been climbing. The problem of restructured assets has also been increasing over recent quarters. The total value of restructured loans in bank books under the corporate debt restructuring facility was an estimated Rs.2.29 trillion in March. There are an additional Rs.1.7 trillion of loans that have been restructured on a bilateral basis between individual banks and their troubled borrowers, according to unofficial estimates.

Such restructured loans as well as the usual bad loans now weigh down bank balance sheets.

The recent moves to raise the cost of loan restructurings—or the withdrawal of regulatory forbearance—is an implicit signal from the central bank that problem loans will not disappear in a jiffy. It usually makes sense to give lenders breathing space to put their loan books in order when companies are hit by a temporary downturn. A few quarters of leniency can help companies get back to their loan repayment schedules quickly. But it is now increasingly clear that the Indian economy is in the midst of a long slowdown, so banks will need to be far tougher with problem loans.

The rise in problem loans should not come as a surprise. It is the inevitable aftermath of a credit boom, as is the case in other economies as well. Loan growth in India was around twice of nominal gross domestic product in the years that immediately preceded the 2008 crisis, a sure sign of effervescent lending. Part of this unusual buoyancy in lending can be explained by the decisions taken within banks but the pressure from New Delhi to step up lending in those exuberant years was also a factor. This is the moment of the inevitable hangover.

What now? A quick improvement seems unlikely. First, it seems that India has still not seen the bottom of the credit cycle. Second, the standard metrics on the ability of companies to service their debt (such as interest cover and free cash flow) are also flashing amber. Third, a sharp reduction in interest rates seems unlikely despite the unexpectedly sharp drop in inflation in recent months. Our assessment is that asset quality in Indian banks will continue to deteriorate for at least a few more quarters (though rising bond prices as a result of a fall in long-term yields could provide some buffer to banks that collectively own more than a quarter of their assets in bonds).

The asset quality of banks is closely related to the state of the underlying economy, which is now in the midst of a structural slowdown. The recent regulatory tightening should be examined against this backdrop, as a recognition of the true state of the Indian economy.

Investors too should welcome the stricter measures, because the regulatory forbearance we saw after 2009 was an attempt to postpone the day of reckoning, when a bank has to take a hit from its problem loans.

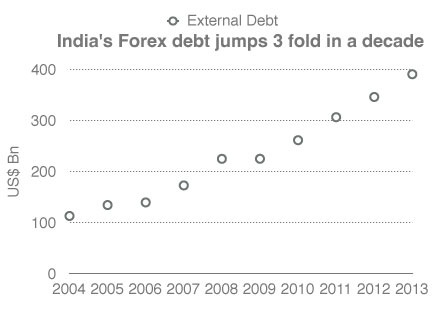

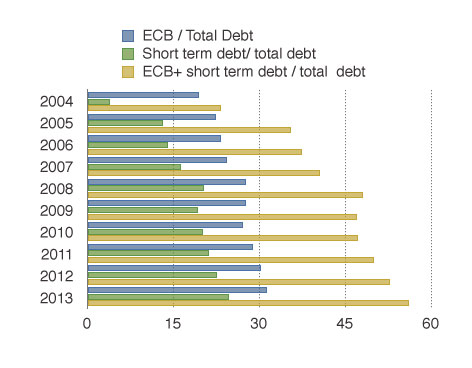

FDI inflows declining and rupee depreciating

http://www.thehindu.com/business/Economy/fdi-dips-by-38-to-224-bn-in-201213/article4775276.ece

Government’s efforts to promote India as an investment destination does not seem to be yielding fruits as FDI inflows registered 38 per cent decline to $22.42 billion in 2012-13 compared to the previous year.

FDI inflows were worth $35.12 billion in 2011-12.

The government had taken several policy decisions in the past few months to attract foreign investments. Important among these include allowing FDI in multi-brand retail and civil aviation sectors and seeking legislative approval for increasing FDI cap in insurance and pension sectors.

In March this year, the country had attracted $1.52 billion FDI, taking the total to $22.42 billion in the entire financial year, an official in the Department of Industrial Policy and Promotion (DIPP) told PTI.

Sectors which received large FDI inflows during 2012—13 include services ($4.83 billion), hotel and tourism ($3.25 billion), metallurgical ($1.46 billion), construction ($1.33 billion), automobiles ($1.53 billion) and Pharmaceuticals ($1.12 billion), the official added.

India received maximum FDI from Mauritius ($9.49 billion), followed by UK ($7.87 billion), Singapore ($5.25 billion), Japan ($2.97 billion) and United States ($1.11 billion).

According to industry experts, there is a need to improve business environment in the country.

In November 2012, India attracted FDI worth $1.05 billion, which was two—year low.

India would require around $1 trillion in the next five years to overhaul its infrastructure sector such as ports, airports and highways to boost growth.

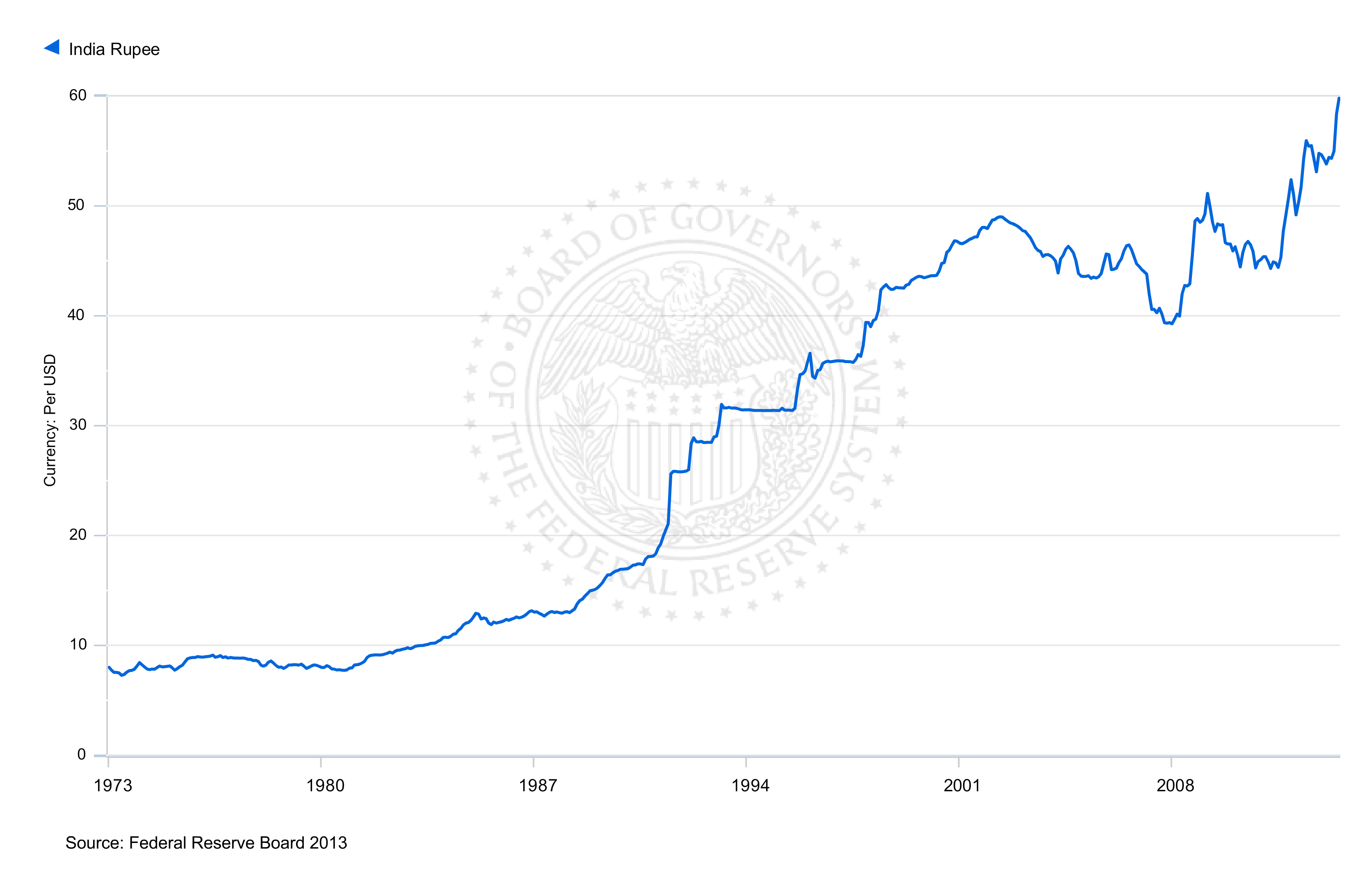

Decline in foreign investments could put pressure on the country’s balance of payments and may also impact the value of the rupee.

Rupee declined by 12 paise to end at 11—month low of 56.50 against the US dollar on Friday amid worries over current account deficit and GDP growth.

With FII outflows of $90 million in stocks, RBI’s poor inflation outlook and GDP growth rate falling to decade’s low of 5 per cent pushed the rupee downwards to 56.76 — its lowest since June 28, 2012.

Economic growth rate slipped to a decade low of 5 per cent in 2012—13 due to poor performance of farm, manufacturing and mining sectors.

GDP growth in Jan- March is a mere statistical growth due to base affect ?

http://www.livemint.com/Opinion/DuHmUO6Inoyspt254OeGWJ/GDP-growth-improves-a-tiny-bit-aided-by-smoke-and-mirrors.html

Has the economy turned the corner? That’s the big question the gross domestic product (GDP) numbers were supposed to answer. Has it indeed bounced off a bottom? At first glance, the answer to that question seems to entirely depend on your measuring rod. For instance, if we take the quarterly estimates of GDP at 2004-05 market prices from the expenditure side, we find real GDP growth was 3.4% in the June quarter, 2.5% in the September quarter, 4.1% in the December quarter, and 3% in the March quarter. By that yardstick, the economy hit a bottom in the September quarter of 2012-13, bounced back in the next, and then fell back again in the March quarter. The rather dubious consolation is that this yardstick is well known to be dodgy and the credibility of the expenditure-side GDP figures is rather low.

Going back to the more credible GDP data at factor cost, we find growth was 4.8% in the March quarter, a mite higher than the nadir of 4.7% reached in the preceding quarter. That would indicate that the economy has indeed bounced off a bottom, a very weak bounce, more of a twitch really.

The problem, as usual, lies in the base effect. It’s true that real GDP growth at factor cost was 4.7% in the third quarter and 4.8% in the fourth quarter compared with a year ago. That 4.7% growth was on top of 6% growth in the third quarter of 2011-12, while the 4.8% growth was on top of a much-lower 5.1% growth in the fourth quarter of 2011-12. Even the feeble bounce was entirely statistical.

The same holds true for several of the sectors. Growth in manufacturing, for example, has moved up slowly and steadily from minus 1% in the first quarter of 2012-13 to 2.6% in the fourth quarter. That looks like a decent recovery. The problem is that in the first quarter of 2011-12, manufacturing growth was 7.4% and it was a mere 0.1% in the fourth quarter of that year. In short, the entire credit for the growth in manufacturing goes to the base effect.

Apart from agriculture, with its seasonal vagaries, are there any sectors that have bucked the base effect? The financing, insurance, real estate and business services segment seems to have done just that. It grew by 9.1% in Q4, 2012-13, on top of 11.3% growth in the year ago quarter. Compare that to its much-lower 7.8% growth in Q3, 2012-13, on top of 11.4% growth in the year ago quarter.

On the other hand, there are several sectors that have done badly in spite of a favourable base effect. Consider electricity, gas and water supply, whose growth rate has gone down from 4.5% in the third quarter of 2012-13 to 2.8% in the fourth, although growth in this sector in Q4 of the previous year was much lower than in Q3 that year. This clearly shows the impact of supply-side problems in the power sector. Similarly, growth in trade, hotels, transport and communication slackened a bit in the fourth quarter compared with the third, despite a favourable base effect. Community, social and personal services, a proxy for government expenditure, unsurprisingly saw tepid growth as the fiscal deficit came down.

How much did the different sectors of the economy contribute to GDP growth in 2012-13? As much as 35% of the growth was generated by the trade, hotels, transport and communication sector, closely followed by financing, insurance, real estate and business services, which accounted for 31.3%. The community, social and personal services segment contributed 16.8% of the growth. It means these three service sectors contributed a huge 83.1% to growth last fiscal year.

Contrast the miserable performance of manufacturing, which accounted for a mere 3.3% of growth. The construction sector contributed more than double that. As a matter of fact, agriculture, forestry and fishing generated 5.4% of last year’s growth, more than the share of manufacturing. The contribution of the mining sector was negative, because of the court-directed closure of mines. The chart shows the contribution from the different sectors. Clearly, mining is the weakest link, closely followed by manufacturing.

The Central Statistical Organisation also seems to have been bang on target with its estimate of 5% real GDP growth at factor cost for 2012-13. A closer examination shows, however, that it had overestimated growth in manufacturing, mining, electricity, gas and water supply and, to a minor extent, in community, social and personal services, and underestimated growth in trade, hotels, transport and communication. That the overall growth rate came out exactly as it predicted can be attributed to an extraordinary stroke of luck.

India’s growth slows down – India is running out of fuel ?

http://timesofindia.indiatimes.com/business/india-business/Its-official-Indian-economy-slowed-to-a-10-year-low-of-5-in-2012-13/articleshow/20374920.cms

The Indian economy grew at its slowest pace in a decade in 2012-13, posing another fresh challenge for the UPA coalition to revive growth and boost sentiment ahead of the general elections next year.

Data released by the Central Statistical Organization (CSO) on Friday showed that the economy grew 5% in 2012-13, compared to 6.2% expansion in the previous year. It was in line with the advanced estimates released earlier.

The economy grew 4.8% in the January-March period, the fourth quarter of the 2012-13 fiscal year, marginally above the upwardly revised 4.7% expansion in the previous quarter, providing some hope of a tentative turnaround. But the overall economic scenario still remains challenging and the GDP data should come as a wake-up call for the government.

The CSO numbers are also an embarrassment for the finance ministry which had questioned the statistics office’s methodology and expressed doubts about the advanced estimates.

The finance ministry had slammed the CSO for forecasting 5% growth for 2012-13. Finance minister P Chidambaram had said the estimate of 5% was based on “dated data”. He had said that growth would be closer to 5.5% and had exuded confidence that green shoots of recovery were visible in the economy.

The high current account deficit, which widened to 6.7% in the December quarter, and stubborn inflation has acted as obstacles to easing monetary policy aggressively. While the Reserve Bank of India has cut interest rates it has cautioned about the persisting inflationary pressures and risks still facing the economy.

What has been most disappointing is that industrial output growth in 2012-13 has been a mere 1%, posing a threat to job creation and overall growth.

Friday’s data showed the farm sector rose 1.9% in 2012-13 compared to 3.6% in the year-ago period while the crucial manufacturing sector grew 1% compared with 2.7% expansion in 2011-12.

The services sector, which accounts for nearly 60% of the economy, rose 7.1% in 2012-13 compared to 8.2% growth in the year-ago period.

CDR gives an indication that the corporate sector is crashing !

http://www.livemint.com/Industry/h7u6wQngeSZ6jL8MfCBpGL/Restructured-loans-cross-227-trillion-pace-slows.html

The latest data from the CDR cell suggests that Indian banks added Rs. 15,016 crore of restructured loans in the March quarter, about Rs. 9,000 crore less than what they had done in the pre ceding quarter. On a cumulative basis, total restructured loans crossed Rs. 2.27 trillion, or 4.4% of the total loans given by Indian banks.

Indian banks have been hit by a surge of bad loans in the face of declining economic growth, estimated at a decade’s low of 5% in the year ended 31 March, project delays and high interest rates that have made it difficult for borrowers to repay debt. Lenders have been easing repayment terms to avoid classifying them as bad assets.

The CDR numbers do not reflect the actual pile-up of restructured loans in the banking system because lenders also recast loans outside the CDR platform, on a bilateral basis.

The aggregate figure for bilateral loan recasts is not available, but bankers said such recasts may nearly equal the CDR figure. That would take the total restructured assets of the Indian banking industry to around Rs.4 trillion.

In the whole of fiscal 2012-13, Indian banks restructured a total of Rs.77,101 crore of loans through the CDR route, nearly double the amount in the previous fiscal (Rs.40,000 crore). Analysts expect about 25-30% of such loans to turn bad.

Iron and steel contributed most to the restructured loan pile—23%—followed by infrastructure (9.65%) and power (8.13%). The textile, telecom and fertilizer sectors, and non-banking finance companies, too, are high on the list.

Despite a decline in the CDR numbers in the March quarter, bankers and financial sector analysts are sceptical about a sustainable revival at Indian companies. The pain associated with mounting bad loans is unlikely to ease at least in the next six months, they said.

Gross non-performing assets (NPAs) of 40 listed Indian banks rose to Rs.1.79 trillion in December fromRs.1.25 trillion a year ago, an increase of 43.1%. In the past, the Reserve Bank of India (RBI) had cautioned banks about the need for enhanced risk assessment tools to monitor loan quality.

Factory output shrinks 1st time in over 4 years .

http://in.reuters.com/article/2013/06/03/india-manufacturing-pmi-idINDEE95203N20130603

The sombre PMI findings came hard on the heels of data released on Friday that confirmed Asia’s third largest economy grew at its slowest pace in a decade in the fiscal year that ended in March.

The overall HSBC Manufacturing Purchasing Managers’ Index (PMI), which gauges business activity in Indian factories but not its utilities, sank to 50.1 in May from 51.0 in April, and was the third straight monthly fall.

Though the May reading was the lowest since March 2009, the overall index has held above the watershed 50 level that divides growth from contraction for over four years.

The reading for the factory production sub-index, however, showed output contracted in May from a month earlier as new orders growth slowed to a trickle. The output sub-index fell to 48.6 in May from 50.2 in April.

“Economic activity in the manufacturing sector slowed further in May as output contracted in response to softer domestic orders,” said Leif Eskesen, an economist with survey sponsor HSBC. Eskesen said power outages added to the drop in production

Defaults in Agricultural credit in another bubble ?

http://www.livemint.com/Industry/ph30HumD1FPAGaBj0XCOyH/Kisan-Credit-Cards-Bad-loan-bubble-waiting-to-burst.html

A surge in exposure to farm debt through Kisan Credit Cards (KCCs) could emerge as a risk for India’s state-run banks, according to experts.

Subsidized loans are given to farmers through KCCs by state-owned banks. Until March 2012, the outstanding amount on such loans was Rs.1.6 trillion through 20.3 million cards, as per the latest Reserve Bank of India (RBI) data. This may have risen to around Rs.2 trillion, bankers said.

Bad loans may be piling up at banks, but they don’t reflect on the books as the credit limit on such cards keeps increasing. Even if a borrower fails to pay up and the banks add the unrealized interest to the exposure because of the rising credit limits—typically 10% every year—the so-called capitalization of interest does not affect the status of the loan account.

State Bank of India (SBI) has the largest exposure to KCC loans—about Rs.44,000 crore— and 5% of this has turned bad, the bank said; Central Bank of India’s exposure isRs.8,428.05 crore and that of Bank of Maharashtra is Rs.2,045 crore.

According to RBI data, banks had Rs.33,200 crore overdue in the direct agrifinance portfolio till 2011 June. The latest figures are not available.

The credit culture in rural India deteriorated sharply after the government announced a Rs.70,000 crore debt waiver for farmers in the February 2008 budget.

The farm loan waiver was one of the United Progressive Alliance government’s key programmes in its first tenure and at least partly responsible for its return to power in 2009.

“Outstanding KCC loans have grown at around 33% in past two years while the number of credit cards has grown at around 13%,”

The share of agriculture, which once generated maximum jobs, has been shrinking as a percentage of national income in Asia’s third largest economy—from 35.75% in 1981 to 16.75% in 2012.

Agriculture is one of the largest sources of bad loans for most banks. It is contributing 9.72% to the gross NPAs of SBI and 7% of Central Bank of India. The nation’s largest lender SBI has the largest gross NPAs —Rs.53,457.79 crore, or 5.3% of loans, followed by Punjab National Bank (Rs.13,997.82 crore, or 4.61% of loans), Central Bank of India (Rs.8,938.47 crore, or 5.64% of loans) and UCO Bank (Rs.6,711.29 crore, or 5.53% of loans).

A bad monsoon could mean a dramatic turn for the worse as the June-September rainy season constitutes India’s main source of irrigation.

Brief summary :

- The financial problems of Indian companies are now being reflected in the asset quality of banks that have lent them money.

And the NPA’s are growing every hour.

- Government’s efforts to promote India as an investment destination does not seem to be yielding fruits as FDI inflows registered 38 per cent decline to $22.42 billion in 2012-13 compared to the previous year.

- The Indian economy grew at its slowest pace in a decade in 2012-13

- Industrial output growth in 2012-13 has been a mere 1%, posing a threat to job creation and overall growth.

- Factory output shrinks for the 1st time in over four years

- Farm sector rose 1.9% in 2012-13 compared to 3.6% in the year-ago period while the crucial manufacturing sector grew 1% compared with 2.7% expansion in 2011-12

- The services sector, which accounts for nearly 60% of the economy, rose 7.1% in 2012-13 compared to 8.2% growth in the year-ago period.

- The share of agriculture, which once generated maximum jobs, has been shrinking as a percentage of national income in Asia’s third largest economy—from 35.75% in 1981 to 16.75% in 2012.

- Until March 2012, the outstanding amount on Kisan Credit card loans was Rs.1.6 trillion through 20.3 million cards, as per the latest Reserve Bank of India (RBI) data. This may have risen to around Rs.2 trillion

- “Outstanding KCC loans have grown at around 33% in past two years while the number of credit cards has grown at around 13%,”

10. Gross non-performing assets (NPAs) of 40 listed Indian banks rose to Rs.1.79 trillion in December fromRs.1.25 trillion a year ago, an increase of 43.1%.

11. The total restructured assets of the Indian banking industry could be around Rs.4 trillion.

12. All the emerging or the sunrise industries are not earning enough to pay loans and this clearly shows that India is a oversold story . Iron and steel contributed most to the restructured loan pile—23%—followed by infrastructure (9.65%) and power (8.13%). The textile, telecom and fertilizer sectors, and non-banking finance companies, too, are high on the list.

13. Eurozone is passing through a crises that could worsen, and impact the Indian exporters

14. Rupee is depreciating, and is the worst performing currency in Asia

Overall, I stand by my assessment of the Indian economy in March 2012 (https://commonmansblog.com/2012/03/22/have-we-oversold-the-india-story/ ) and in October 2012 (https://commonmansblog.com/2012/10/11/india-from-emerging-to-a-submerging-economy/ )that India is an oversold story and should prepare for the worst times ahead . Also, I said on my blog in March about India facing a security threat , and we know what China did (https://commonmansblog.com/2013/03/03/economy-downgrade-and-downfall-both-are-a-foregone-conclusion/) .

I see no reason to believe that India will be back to normal before 2015-16, and that too, provided politicians become realistic . In the current environment , none of the political parties or the politicians have a plan to salvage the situation, and my prediction is , that India’s growth rate might fall below 4 % . The Indian Titanic is in mid of a turbulent sea, heading towards a more severe storm . The Titanic is sinking . Can we do something ?

Rajendra Pratap Gupta

http://www.commonmansblog.com